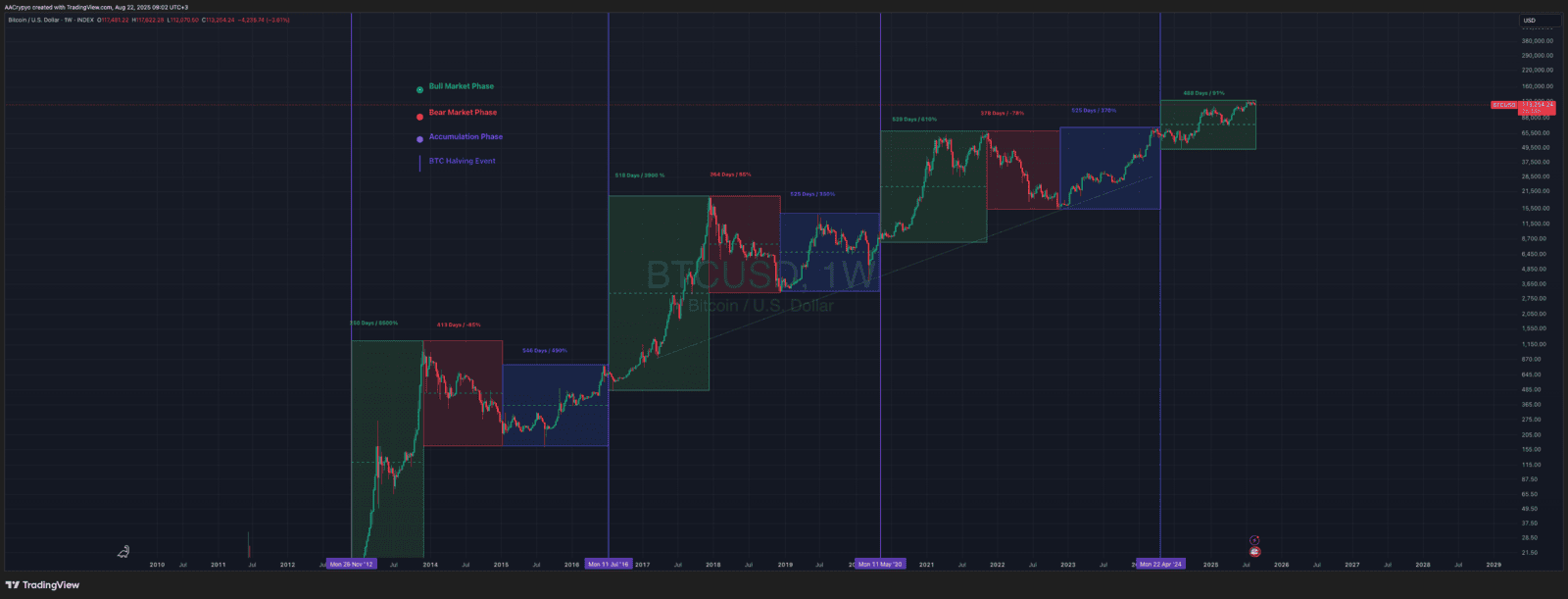

One of the hardest parts of investing is knowing when to take profits, exit positions, or rotate into something new, especially during a bull market when everything seems to be performing well. We are now deep into the current cycle. The last major low was almost three years ago, and the most recent Bitcoin halving took place nearly 500 days ago. History suggests this places us in the latter stages of the cycle.

The question feels more relevant than ever given recent price action and shifting sentiment. Some argue the market has already topped and that a new bear phase is beginning, pointing to past cycles as evidence. In the previous cycle the major collapses were FTX, Luna, Three Arrows Capital and a string of other hedge funds. This time attention has turned to Bitcoin treasury companies, which critics claim could be the next domino to fall, accusing them of relying on what they call “paper Bitcoin.”

Are these concerns valid, or simply another fear-driven narrative? And beyond that, what does 2026 hold: another bullish leg, or the start of a prolonged bearish phase?

Does the Four-Year Cycle Still Hold?

For Bitcoin’s entire existence it has followed a repeating pattern often referred to as the four-year cycle. In this framework, Bitcoin experiences three years of bullish price action followed by a fourth year of decline, with each cycle typically kicked off after a halving event, which occurs roughly every four years. Historically, Bitcoin has also tended to reach its cycle high around 500 days after the halving. The chart below shows a visual of this four-year rhythm and the time it has historically taken from each halving to the subsequent cycle peak. Of course, past performance does not guarantee future results.

This cycle appears to be following the same structure, although there has been debate about whether Bitcoin has moved beyond its traditional pattern. Some argue that the four-year cycle may lose relevance as adoption grows and that future market behaviour will be shaped more by external factors than by halvings. The reasoning is that Bitcoin has reached a level of maturity where major individuals or institutions can move the market more than the programmed supply schedule. For instance, the influence of Donald Trump through social media commentary, executive orders, or pro-crypto policy, has had visible effects on price. Similarly, corporate leaders such as MicroStrategy’s Michael Saylor or BlackRock’s Larry Fink could have outsized impact. A large sale by Saylor or an announcement that BlackRock was allocating even 1 percent of its holdings into Bitcoin would likely move markets more than the latest halving. This does not mean halvings no longer matter, only that their effect diminishes with each cycle. Over time, Bitcoin’s maturity and adoption may see it trade more in line with broader risk assets like the S&P 500 rather than its own halving-driven rhythm.

Despite these arguments, Bitcoin still appears to be playing out the four-year cycle in real time. The most recent halving took place on 20 April 2024, which was 488 days ago, bringing us very close to the 500-day mark. Bitcoin has also been in an uptrend for nearly three years since its 2022 cycle low. These factors are why some market watchers suggest the recent move to 124k may mark the cycle top, or at the very least that the peak is near, in line with the historical four-year pattern.

2021 vs Today: Is History Rhyming or Repeating?

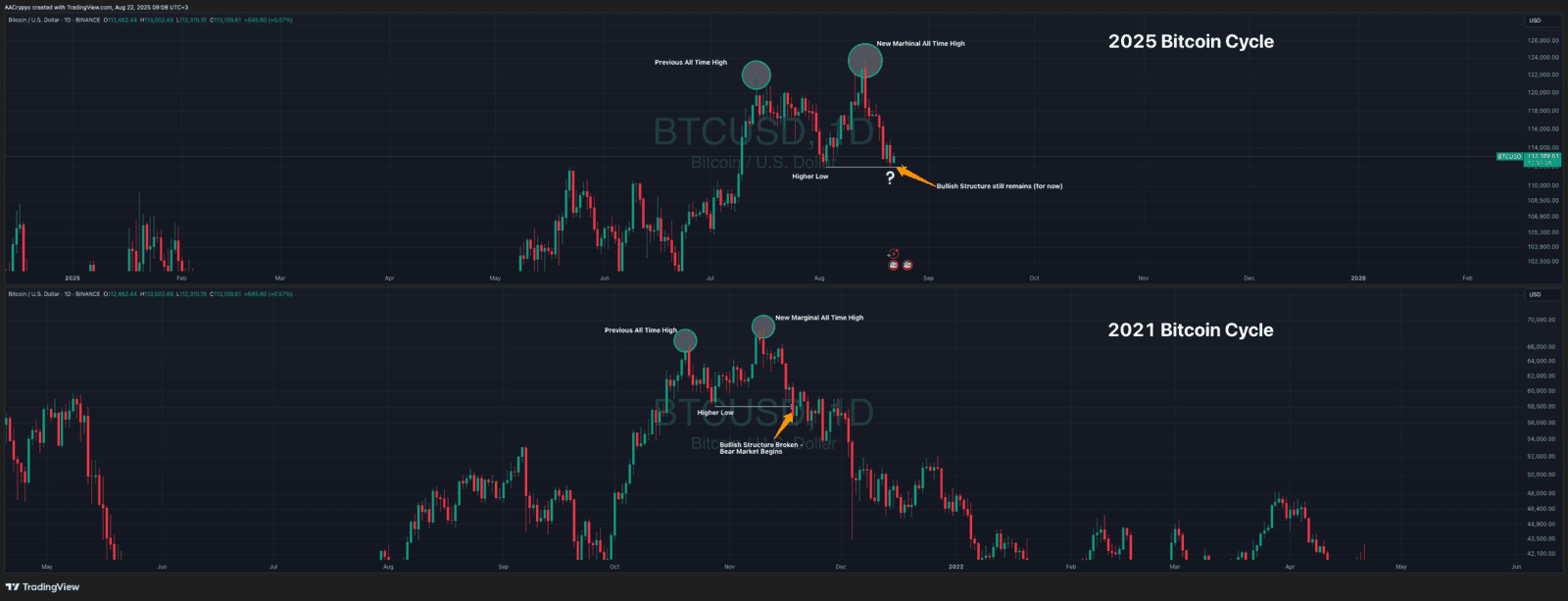

You would think that after setting an all-time high sentiment would be bullish and firmly in the greed zone, but only a week later the mood has shifted. Many are now saying the rally is over and are pointing to the 2021 cycle as proof. So it is worth looking back at what happened then to see if the comparison holds weight.

The main concern is that the latest all-time high was only marginally higher than the previous one. We saw the same pattern in 2021. On 20 October 2021 Bitcoin hit a new all-time high just below 67k before pulling back, forming a higher low, and then pushing to a fresh all-time high of 69k on 10 November. That move only beat the earlier high by less than 3 percent. The marginal new high turned out to be the top, as it was followed by a breakdown of the bullish structure and the beginning of the bear market.

Fast forward to today and the similarities are striking. The previous all-time high was set at 123k on 14 July, followed by a pullback that held support at just under 112k, creating a higher low. Price then rallied again, reaching a new all-time high of 124.5k on 14 August. Just like in 2021, the new high was only marginally above the last, and sentiment quickly turned bearish. Price action is now threatening to make a lower low, which would confirm a break in the bullish structure.

History does not repeat exactly, but it often rhymes. If Bitcoin falls and forms a lower low it would strengthen the bearish case and cement negative sentiment. If instead it makes a higher high, that would nullify the bearish view and reinforce the bullish structure.

This cycle's FTX or 3AC collapse?

In the last cycle, we witnessed the collapse of hedge funds, trading firms and exchanges that were considered too big to fail until they weren’t. The unraveling of 3 Arrows Capital, Alameda Research and ultimately FTX dealt brutal blows to the market during the bear phase, sending Bitcoin and broader crypto markets even lower. A common thread ran through these failures: they were overleveraged and in many cases trading with borrowed or misused funds. When the bear market deepened and drawdowns accelerated, they fell like dominoes.

This cycle, the spotlight has shifted. Some critics argue that Bitcoin treasury companies, firms holding large amounts of Bitcoin on their balance sheets, could become the “FTX or 3AC” of this era, vulnerable to collapse and capable of amplifying downside pressure on Bitcoin’s price.

The Bitcoin treasury model has been championed by MicroStrategy CEO Michael Saylor. Under his leadership, the company has accumulated a vast Bitcoin reserve by purchasing BTC directly and then raising more capital through convertible notes or equity offerings to buy even more. In some cases, debt financing is also used, which increases the risk profile of the strategy. While companies like Tesla and Block used internal funds rather than debt to acquire their Bitcoin, MicroStrategy’s approach is unique in its scale and reliance on leverage. More recently, other Bitcoin-focused businesses have signalled similar intentions, inspired by Saylor’s model, though none yet match its aggressiveness.

The main concern revolves around leverage and debt sustainability. MicroStrategy alone has issued billions of dollars in debt to accumulate Bitcoin. The risk is clear: if a deep bear market sends Bitcoin sharply lower, the value of these corporate treasuries could fall to the point where companies struggle to service or refinance their debt. In a worst-case scenario, this could lead to forced liquidations of Bitcoin holdings, sparking major sell-offs and accelerating price declines. So far, MicroStrategy’s strategy has survived one full bear market, but as the model expands and imitators emerge, critics warn that it only takes one large failure to destabilise the market temporarily.

Even if a Bitcoin treasury company fails and is forced to liquidate, it is important to remember that these companies are separate from Bitcoin itself. The underlying Bitcoin network and asset remain unaffected. Prices could certainly fall in the short term, but the fundamental qualities of Bitcoin such as scarcity, security and decentralisation do not change. The analogy to the Global Financial Crisis is useful here. During 2008, financial institutions created risky debt instruments tied to mortgages. When the debt collapsed, markets imploded, but the houses themselves remained intact. Prices fell, but the underlying asset was unchanged. Similarly, if overleveraged Bitcoin treasury companies collapse, the long-term value proposition of Bitcoin itself is not diminished.

Whether or not Bitcoin treasury companies succeed, Bitcoin remains Bitcoin. For long-term investors with conviction, the noise of corporate strategies, leverage and debt cycles should not overshadow the asset’s fundamentals. Price volatility is inevitable, but the core use case and value of Bitcoin persist regardless of how any one company chooses to manage its balance sheet.

2026: Bullish or Bearish?

As 2025 draws to a close, attention naturally shifts to what 2026 may bring. The first eight months of this year have been somewhat underwhelming and have not fully lived up to expectations, leaving investors to wonder what lies ahead. Those who subscribe to the four-year cycle theory argue that 2026 is likely to be a down year for Bitcoin, while others point instead to broader macroeconomic forces that could provide a very different outlook.

Two factors stand out as particularly important for Bitcoin and risk assets more broadly: interest rate cuts and global money supply. When interest rates are cut, borrowing becomes cheaper, economic activity is stimulated and liquidity increases. This tends to drive more capital into investments, including Bitcoin, which is generally positive for its price. Meanwhile, global money supply, often referred to as M2, measures the level of liquidity in the system. As central banks expand money supply, it not only provides more fuel for asset markets but also devalues fiat currencies at the same time, a dynamic that strengthens the investment case for Bitcoin.

With these two influences set to play a central role in 2026, the backdrop looks favourable. Current expectations suggest at least two rate cuts in the second half of 2025 and the possibility of additional cuts in 2026. At the same time, global M2 is continuing to grow, with no signs of contraction on the horizon. Together, these forces create conditions that are historically bullish for Bitcoin and suggest that 2026 could shape up to be a strong year despite cycle-based expectations to the contrary.

What Really Matters for Bitcoin?

Bitcoin’s history has shown us that cycles, sentiment shifts and major market events often repeat in familiar patterns, even if the details change each time. The debate over whether we are nearing the end of this bull run, whether treasury companies could be the next weak link, or whether the four-year cycle still holds, ultimately comes back to the same truth: short-term volatility does not alter the long-term case for Bitcoin.

Bearish sentiment will rise whenever price action stumbles, just as optimism returns when new highs are set. Treasury companies may succeed or fail, but their fate is separate from the Bitcoin network itself. Halvings may play a smaller role as adoption grows, but the asset continues to mature and integrate into the global financial system.

Whether 2026 brings another leg higher or a cooling-off period, Bitcoin’s trajectory is shaped less by short-term narratives and more by its fundamental properties of scarcity, decentralisation and resistance to monetary debasement. For investors with conviction, the question is not whether Bitcoin will have pullbacks or corrections, but whether they have the patience to see beyond them.

Written by Alexandar Artis

Create a brokerage account today

Reach out to us at Stormrake for further market insight and allow us to help you navigate the sea of mania and laser-eye memes, so that you can realise your goals in the market!

No Advice Warning

The information in this newsletter is general only. It should not be taken as constituting professional advice from the author - Stormrake PTY LTD.

Stormrake is not a financial adviser and does not provide financial product advice. You should consider seeking independent legal, financial, taxation or other advice to check how the information relates to your unique circumstances. Stormrake is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by this newsletter.

Disclaimer

All statements made in this newsletter are made in good faith and we believe they are accurate and reliable. Stormrake does not give any warranty as to the accuracy, reliability or completeness of information that is contained here, except insofar as any liability under statute cannot be excluded. Stormrake, its directors, employees and their representatives do not accept any liability for any error or omission in this newsletter or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information provided in this newsletter is owned by Stormrake. You may not alter or modify this information in any way, including the removal of this copyright notice.Copyright © 2024 Stormrake Pty Ltd, All rights reserved