To receive the Morning Note in your inbox, subscribe here: https://stormrake.substack.com/

Over a third of Australian households have just seen their expenses rise over the past 24 hours following the Reserve Bank of Australia’s decision to lift rates by 25 basis points.

While the move was largely expected by major banks and consensus forecasts, the decision itself was far from unanimous, passing in a narrow 5 to 4 vote. That split highlights just how uncertain the current macro environment is. Policymakers are tightening into inflation that is increasingly being driven by forces beyond their direct control.

Domestic demand remains firm, supported by ongoing government spending and consumer resilience, both of which continue to add liquidity into the system. At the same time, external pressures, particularly energy costs linked to geopolitical tensions in the Middle East, are feeding into broader inflation. The result is sticky price growth that rate hikes alone are struggling to suppress.

This is now feeding directly into bond markets. Australian 10 year yields have pushed to their highest levels since 2023, and before that 2008, reinforcing the reality of tightening financial conditions and rising capital costs across the economy.

But beneath the surface, this is ultimately a policy-driven environment.

Central banks, whether it is the RBA, the Fed, or others globally, dictate the value, supply, and issuance of fiat currency. They set borrowing costs, influence liquidity, and adjust monetary conditions in response to evolving economic pressures. These decisions are made by unelected bureaucrats, often reacting to variables that are themselves unpredictable and, at times, outside their control.

For households and investors, this creates a system where financial outcomes are closely tied to policy decisions rather than purely market-driven dynamics.

Roughly 3.4 million households, or around 35%, hold property with a mortgage. While home ownership remains a core financial goal, it also exposes individuals to this policy cycle. As borrowing costs rise, mortgage repayments increase alongside broader living expenses. For those operating with higher leverage, margins compress quickly.

The challenge becomes more pronounced when liquidity is considered. Real estate is inherently illiquid. In periods of stress, exiting positions is neither fast nor guaranteed at favourable pricing, particularly if multiple participants are forced to sell simultaneously.

Contrast that with Bitcoin.

Bitcoin operates on a fixed and transparent monetary framework. Supply is predetermined, issuance follows a clear schedule, and the network is maintained by decentralised validators rather than central authorities. No single entity can adjust its monetary policy in response to short-term pressures.

In a world increasingly shaped by reactive policy decisions, that distinction matters.

So the question becomes, as policy tightens, liquidity contracts, and control remains centralised, what more needs to happen before you reconsider where you store your wealth?

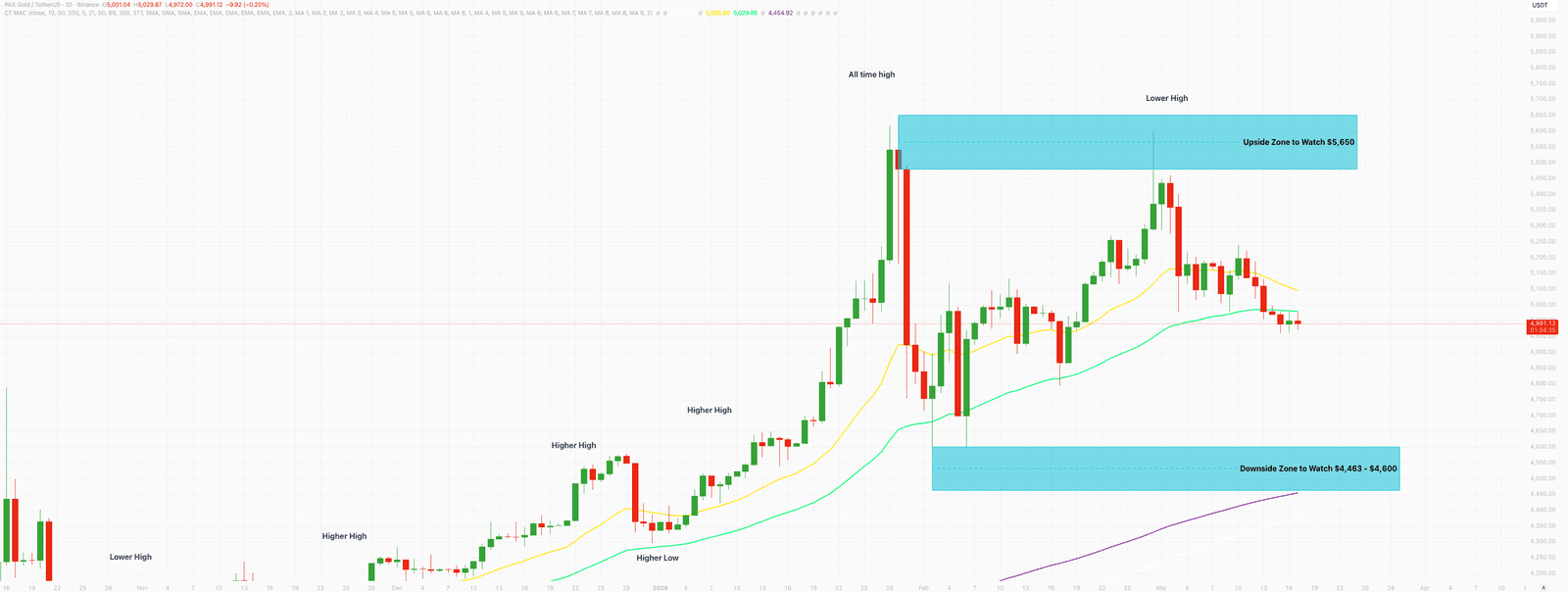

Stormrake Spotlight: Pax Gold (PAXG) ($4,991)

Stormrake Spotlight: Pax Gold (PAXG) ($4,991)