To receive the Morning Note in your inbox, subscribe here: https://stormrake.substack.com/

On 29 June 2026, Strategy officially authorised the first potential Bitcoin liquidation framework in its corporate history. This structural shift marks a profound evolution in corporate treasury management, proving that the aggressive premium model that transformed the firm into the holder of 4.2% of all circulating Bitcoin has encountered its limits. Management has introduced an operational overhaul because the capital allocation flywheel has stalled, exposing the fundamental reality that synthetic proxy wrappers can completely decouple from the spot assets they attempt to replicate.

Across the broader digital asset treasury sector, numerous listed Bitcoin treasury entities now trade at a steep discount to net asset value, reminiscent of the 2022 trust corrections. While the market initially responded positively with MSTR shares jumping 13% as investors welcomed disciplined capital management, the pivot confirms that indirect exposure introduces a layer of financial engineering that will likely end up sub-par when compared to pure Bitcoin performance in the long run.

The Digital Credit Capital Framework

The newly unveiled framework introduces a multi pronged capital allocation model designed to protect corporate structure and defend liquidity. Key adjustments include a $2.55 billion ring fenced cash buffer for debt interest, resetting select preferred dividends to 12.00% to support par value, and two separate $1 billion repurchase authorisations for preferred and common stock.

Crucially, the plan authorises up to $1.25 billion in strategic Bitcoin liquidations, extending total coverage from 17.4 to approximately 25.9 months. This shift formally signals that management now categorises its digital asset stack as active capital for balance sheet defence, moving away from its historical status as an untouchable reserve. These convoluted credit defence mechanisms are entirely unique to the corporate wrapper environment. Investors holding direct spot property require no internal balance sheet choreography, as pure asset exposure is completely insulated from the operational liabilities of an intermediary.

The Reversal of the Equity Flywheel and the Structural Trap

This tactical pivot was forced by severe mathematical constraints that never apply to direct asset holders. While the company’s internal figures place its current mNAV above 1.0, data from CryptoQuant indicates a compression down to 0.76, highlighting the tracking error inherent in synthetic vehicles. When the mNAV flips negative, the corporate model enters a structural trap; every single share sold to acquire more Bitcoin actively destroys 24 cents of value per dollar deployed.

Unlike unencumbered spot property, which maintains a constant 1 to 1 relationship with absolute scarcity, a proxy engine introduces extreme volatility amplification. The firm’s creditworthiness expands when Bitcoin rallies, meaning the vast majority of its debt and equity issuance occurred near cyclical highs, leaving recent purchases underwater. Conversely, almost nothing was accumulated at macro lows. When Bitcoin undergoes a 10% retracement, MSTR equity historically amplifies that drop by roughly 20%. A compressed mNAV then dictates that the entity should liquidate Bitcoin to buy back its own discounted equity, completely reversing the perpetual accumulation thesis and exposing proxy holders to forced structural unwinds.

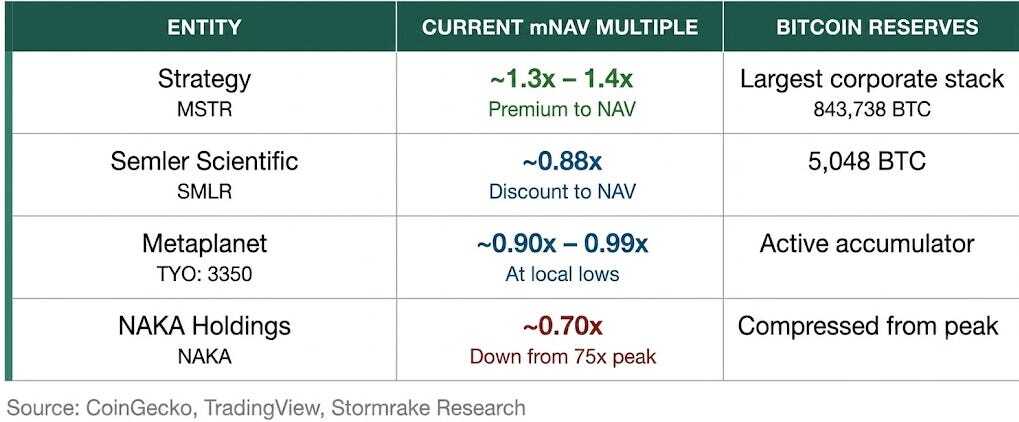

Systemic Treasury Discounts Across the Sector

The evaporation of the treasury premium is a systemic trend affecting the wider Digital Asset Treasury (DAT) landscape, demonstrating that wrapper discount risks are an artificial vulnerability born of structural centralisation.

Up to a third of listed treasury firms now trade below a 1.0x mNAV multiple. If a compressed premium forces these entities into simultaneous, non discretionary selling to service debt, the market will anticipate the flow and front run it, triggering a reflexive downward spiral. This feedback loop has dismantled leveraged crypto structures in prior cycles, yet it remains a risk largely quarantined from those holding direct spot property.

The 2022 Arbitrage Precedent

This dynamic mirrors the structural challenges faced by the Grayscale Bitcoin Trust (GBTC) during the 2022 bear market, when its discount to net asset value widened to a record low near 50% by December. That disconnect proved that a wrapper’s price can completely detach from its underlying asset when a capital raising engine stalls. Strategy is attempting to manufacture its own internal arbitrage mechanism through aggressive buybacks of its discounted paper, rather than waiting for an external market catalyst like an ETF conversion.

Macro Outlook and Desk Execution

Ultimately, attempting to secure exposure to digital asset scarcity indirectly through corporate equity proxies introduces operational liabilities that spot ownership avoids entirely. Corporate proxy models expose investors to board level cash burn, asset liability mismatches, and dilutive capital manoeuvres that degrade the core appeal of owning Bitcoin in the first place.

Direct ownership of spot property offers true asset scarcity and absolute independence from a single balance sheet’s financing decisions. The professional trading desk at Stormrake provides institutional grade execution models to secure unencumbered spot property, ensuring capital allocations bypass corporate wrapper risks and remain entirely within your own control.

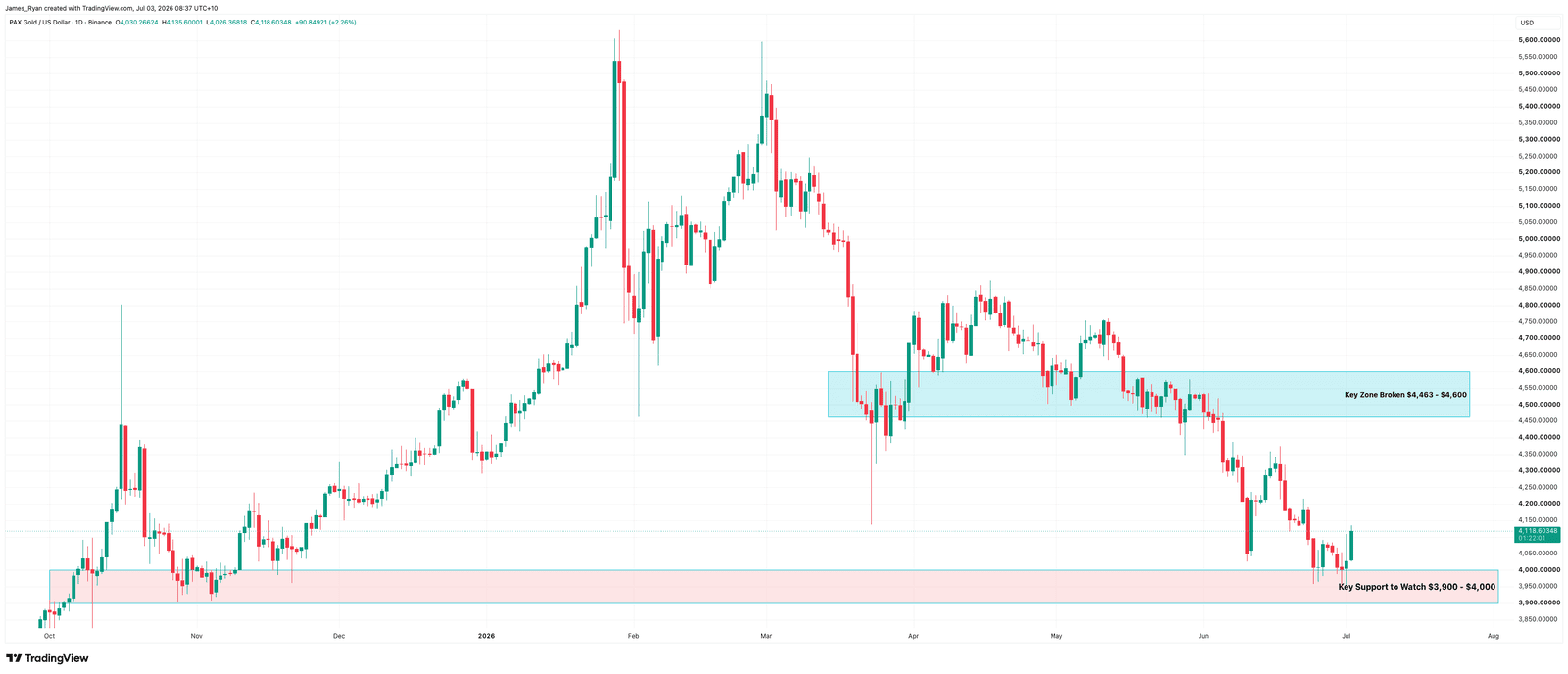

Stormrake Spotlight: Pax Gold (PAXG) ($4,118)

Stormrake Spotlight: Pax Gold (PAXG) ($4,118)