To receive the Morning Note in your inbox, subscribe here: https://stormrake.substack.com/

The financial markets have just completed a historical masterclass in the structural dangers of speculative equity bubbles. On 12 June 2026, SpaceX completed the largest initial public offering in market history, raising $75 billion at $135 per share to a chorus of near-universal retail euphoria. Driven by intense retail momentum, the stock soared to an all-time high of $225.64 by 16 June, briefly vaulting the company past multi-trillion-dollar legacy conglomerates to become the world’s fifth most valuable entity.

Yet, the unwinding of this speculative fervour was as dramatic as its ascent. By 23 June 2026, a rapid succession of corporate and structural shocks triggered a violent 16.4% single-day capitulation, bringing the three-day aggregate loss to nearly $1 trillion in erased market value. With the stock collapsing back to its first-day opening price of $150, market participants who accumulated at the absolute peak were left holding painful losses of approximately 33% in less than a week.

Bitcoin instead of following SpaceX’s return to orbit, has modestly separated from Elon’s trajectory and used its own launch boosters, allowing the apex asset to maintain firm support in the $60,000 range in the face of broader equity uncertainties resurfacing, including a Micron earnings scare overnight.

The Hidden Vulnerabilities of Corporate Balance Sheet Proxies

For macroeconomic allocators, this corporate wipeout provides a clear analytical lens through which to evaluate a common mistake: attempting to secure exposure to digital asset scarcity indirectly through corporate equity proxies. Many investors buy equity in technology companies simply because those corporations maintain Bitcoin on their balance sheets. The SpaceX episode demonstrates that this proxy exposure is fundamentally flawed.

When purchasing corporate shares instead of direct spot property, an investor is completely exposed to centralised human decision-making and underlying operational liabilities. The SpaceX cash burn rate highlights these systemic corporate risks. The company reported a massive net loss of $4.9 billion for the full year of 2025. While the Starlink satellite infrastructure division generated a steady $4.4 billion operating profit, the highly speculative xAI division consumed those inflows entirely, burning through $6.36 billion in operating losses against a massive $12.7 billion in capital expenditure. By Q1 2026, consolidated net losses accelerated to $4.28 billion.

Furthermore, equity holders are perpetually vulnerable to board-level decisions, such as the sudden announcement of a dilutive $60 billion all-stock acquisition of Cursor immediately following the public listing. This corporate action, combined with a subsequent $20 billion bond offering, signalled clear underlying structural stress. Equity proxies also remain subject to massive supply shocks, such as the impending December 2026 lock-up expiry which will release 96% of currently locked shares onto the open market.

The Cryptographic Alternative: Real Scarcity

Bitcoin’s decentralised architecture is completely immune to these corporate vulnerabilities. The protocol has no centralised board of directors to execute dilutive acquisitions, no capital expenditure overheads to create multi-billion-dollar operating losses, and no corporate debt facilities to service. Its immutable supply cap of 21 million units cannot be expanded by legislative or corporate decree.

This structural integrity is precisely why Bitcoin remains the best-performing asset in recorded economic history. Over a full ten-year macro cycle, Bitcoin achieved cumulative gains exceeding 26,900%, outperforming the S&P 500’s 193% and gold’s 125% by orders of magnitude. On an annualised basis, Bitcoin has returned roughly 230%. Capturing this performance requires deep patience across multi-year cycles. Cyclical corrections frequently experience temporary drawdowns within the 50% - 70% range or greater, yet the underlying market structure has always resolved into higher ranges of secular support.

True wealth preservation requires eliminating unnecessary counterparty risk. Direct ownership of unencumbered spot property offers a mathematical escape hatch from legacy corporate dilution. Connect with a Stormrake broker today to discuss how Bitcoin is “T-minus not long to go now” before its launch into the stratosphere begins, and never looks back.

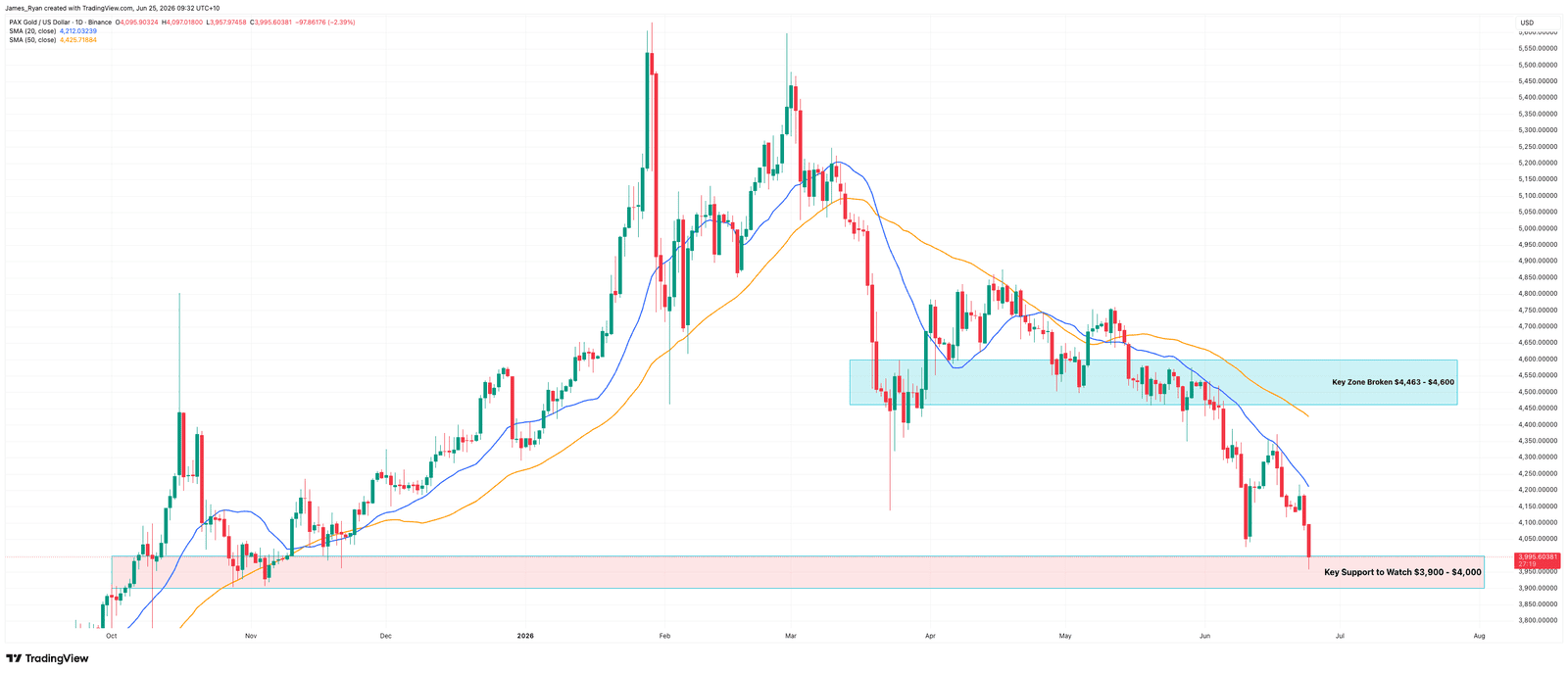

Stormrake Spotlight: Pax Gold (PAXG) ($3,995)

Stormrake Spotlight: Pax Gold (PAXG) ($3,995)