Capitalising the War Machine: Three Case Studies of Debt Expansion

To properly evaluate how overseas engagements dilute domestic purchasing power on a multi year delay, savvy market participants can review historical data. When a superpower issues trillions of dollars in fresh credit for global military operations, the economic distortions appear on a lag. Here is how three major overseas operations over the last few decades have directly reshaped the domestic monetary landscape of the United States:

1. The Gulf War (1990)

Total Financial Cost: The conflict required approximately $61 billion in direct resources. Although international partners subsidised over 80% of the baseline operational costs, the domestic credit strain contributed to a sharp economic recession.

Domestic CPI Projections: Five years after the conflict commenced in 1995, the domestic consumer price index registered at 2.8%. By the 10 year milestone in 2000, prolonged structural adjustments and global energy volatility pushed annual inflation up to 3.4%.

2. The War in Afghanistan (2001)

Total Financial Cost: According to comprehensive data evaluated by the Watson Institute Costs of War Project, the ultimate bill for the 20 year campaign reached an astounding $2.26 trillion.

Domestic CPI Projections: Five years post invasion in 2006, the consumer price index registered a hot 3.2%. Ten years later in 2011, despite the massive macro deflationary shock of the global financial crisis, aggressive central bank credit interventions and sustained war funding kept annual inflation firmly at 3.2%.

3. The Iraq War (2003)

Total Financial Cost: Direct combat operations and subsequent regional reorganisation projects quickly ballooned past $2 trillion in committed capital.

Domestic CPI Projections: Five years into the occupation in 2008, significant systemic market distortions and raw commodity pricing shocks drove domestic CPI to a peak of 3.8%. Ten years later in 2013, following a decade of intense credit expansion, inflation cooled to 1.5% as the credit excess was temporarily absorbed back onto the central bank balance sheet via prolonged quantitative easing programmes.

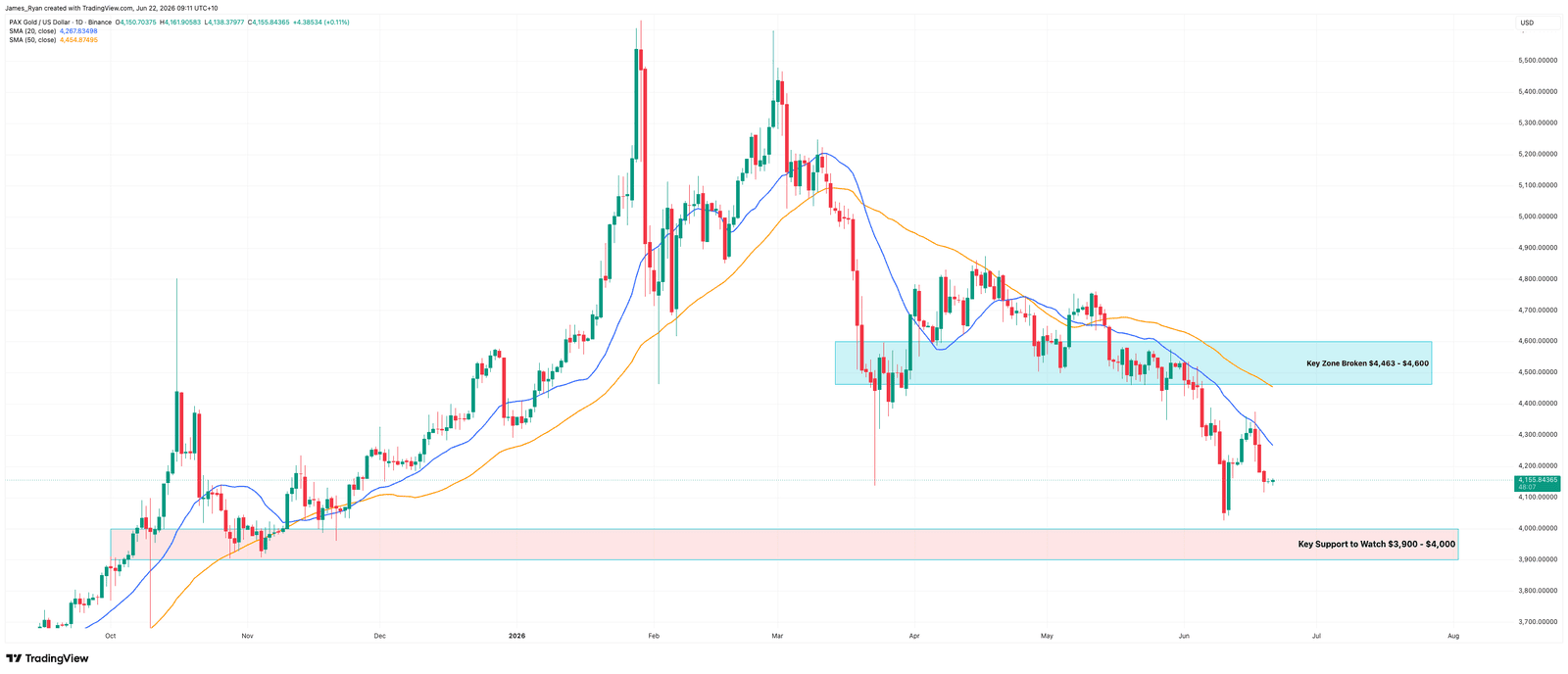

Stormrake Spotlight: Pax Gold (PAXG) ($4,155)