From All Time Highs to Bear Market Calls

From All Time Highs to Bear Market Calls

From All Time Highs to Bear Market Calls

August was a month of extremes for Bitcoin, with fresh all-time highs, sharp reversals, and a whale-triggered sell-off that shook sentiment. The cycle clock is ticking, and with rate cuts approaching and macro conditions shifting, the question now is whether the market has one more leg higher or if the top is already in.

A Month of Extremes: New Highs, Whale Dumps, and Macro Whiplash

They say the best thing you can do after buying Bitcoin is forget about it and come back in ten years. You miss the euphoric rallies and the soul-crushing drawdowns, but when you zoom out a decade later, odds are you are sitting on something worth significantly more than what you paid.

But for many, the volatility in between is part of the appeal. It draws speculators in, even as seasoned Bitcoiners grow numb to it. This August, that volatility was back in full force.

Coming into the month, two factors were expected to shape price action: the ongoing geopolitical tension between Ukraine and Russia, and the latest US inflation data. Both played their part. But the most dramatic twist came from a whale no one saw coming.

August began, like much of the year, with macro tensions. Putin floated a fresh ceasefire proposal that was swiftly dismissed by Zelenskyy. Reports of progress surfaced, with a potential trilateral meeting between Trump, Zelenskyy and Putin discussed. Nothing came of it in the end, but the market moved quickly. Bitcoin surged to a fresh all-time high above $124K following inflation data.

Ironically, while Bitcoin was created to hedge against inflation, it now reacts directly to inflation prints, rate cut speculation and the words of one man: Jerome Powell. As Bitcoin continues to mature, its correlation with traditional markets is strengthening. The same forces moving equities are moving crypto.

The first major driver was CPI. It came in slightly better than expected and gave Bitcoin the momentum to break out and push to new all time highs. But just days later, PPI told a very different story. The hotter-than-expected print triggered a sharp sell-off in risk markets. Bitcoin tumbled. Then Powell spoke.

Arguably the most influential voice in markets right now, Powell delivered a dovish tone in his policy speech that sent risk assets flying. Bitcoin rallied hard and attempted to reclaim the lost momentum post PPI data. It looked like momentum was back. Then the second domino fell.

A Bitcoin whale offloaded 24,000 BTC the day after Powell’s speech. That single move, worth $2.7 billion at the time, wiped over $4,000 off the price in a matter of minutes. As large as that number is, it was just a fraction of this whale’s holdings. They still have around 150,000 BTC sitting in their wallet. For comparison, last month eight wallets moved 80,000 BTC and triggered another market drop. If this whale ever decides to clear out their entire bag, the short-term impact would be massive. But for long-term buyers with patience, those kinds of moves could offer generational entry points.

Is Time Running Out for the Bull Run?

Is Time Running Out for the Bull Run?

It’s the uncomfortable question that tends to get louder as prices climb higher: are we nearing the end of the bull run?

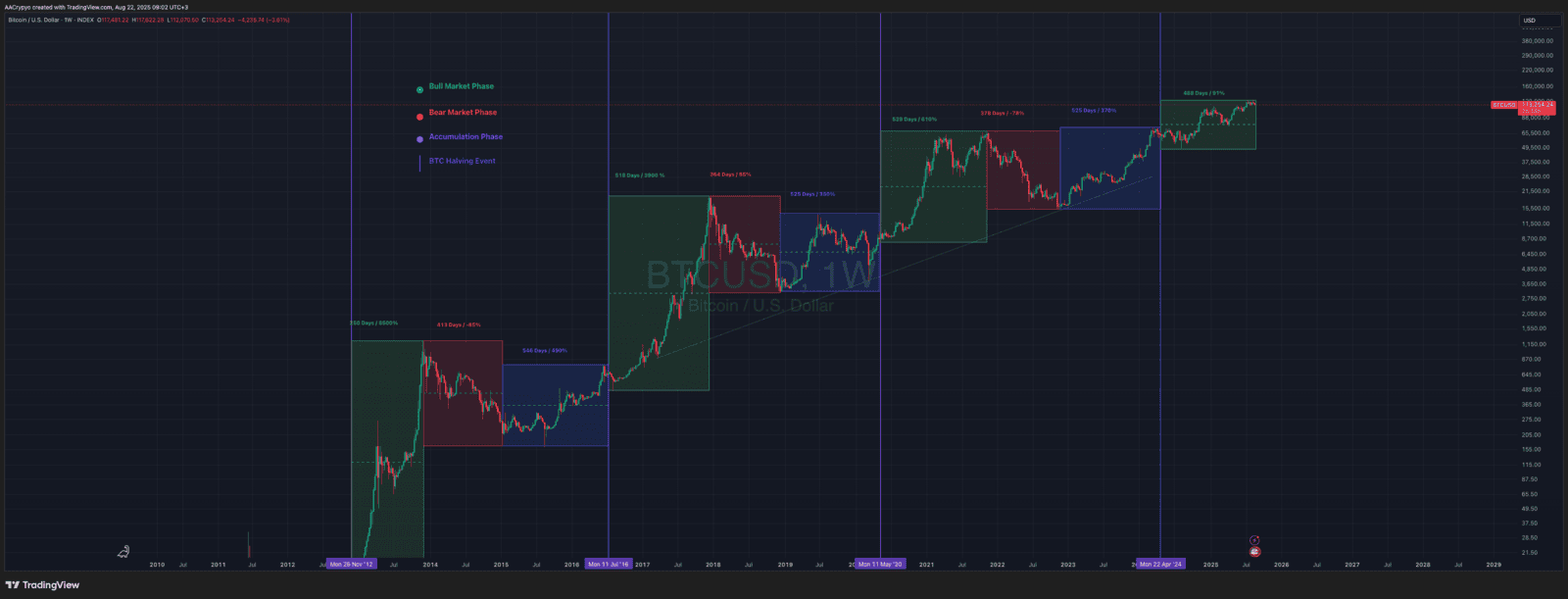

Bitcoin has now spent nearly three years climbing out from its 2022 cycle low, following a rhythm that long-time holders know well. This market structure, often referred to as the four-year cycle, has defined every major bull and bear market since Bitcoin’s inception. The premise is simple. A halving triggers a multi-year rally, followed by a year-long cooldown. Historically, cycle tops have formed around 500 days after each halving.

Right now, we are 490 days out from the most recent halving on 20 April 2024. Bitcoin recently tagged $124K and is beginning to show signs of slowing. That puts us right in the historical window where previous tops have occurred. The chart below shows the time elapsed between each halving and its corresponding cycle peak. Once again, Bitcoin appears to be tracking the same cadence.

Still, a growing school of thought argues that this time could be different. As Bitcoin continues to mature and becomes more integrated into institutional portfolios, the four-year cycle may be losing relevance. In this view, price action is becoming less about the halving and more about macro trends, liquidity flows and key narratives.

Trump’s influence, for example, whether through social media posts, executive orders or pro-crypto policy shifts, has had visible effects on Bitcoin’s price. Similarly, high-profile players like Michael Saylor and Larry Fink can move markets. If BlackRock were to announce even a 1 percent allocation across its products, Bitcoin would likely reprice well before any halving-driven supply dynamics had a chance to kick in.

That’s not to say halvings no longer matter. Their impact just seems to be fading with each cycle. Bitcoin is maturing. Liquidity is deeper. And price behaviour is starting to look more like a high-beta risk asset than a niche inflation hedge. Correlation with the Nasdaq and S&P 500 continues to rise, and policy decisions from the Fed or Treasury are now setting the tone for short-term price direction.

Even with these changes, this current cycle still looks and feels a lot like the previous ones. The timing, structure and sentiment all point toward a market nearing its peak. Some are already calling a top, while others believe we could still see a final blow-off phase that exceeds expectations. That view depends heavily on sustained risk appetite and continued institutional inflows.

Bitcoin’s history has shown that cycles, sentiment shifts and major market events tend to repeat in familiar ways. The details may evolve, but the patterns often stay the same. Whether this marks the end of the bull run or just the beginning of its final leg, one truth remains: short-term volatility does not change the long-term case for Bitcoin.

August Volatility, September’s Seasonal Struggles

August Volatility, September’s Seasonal Struggles

If you had told someone a month ago that Bitcoin would hit new all-time highs and then, just days later, people would be calling for a bear market, they would have thought you were mad. But that is exactly how August played out.

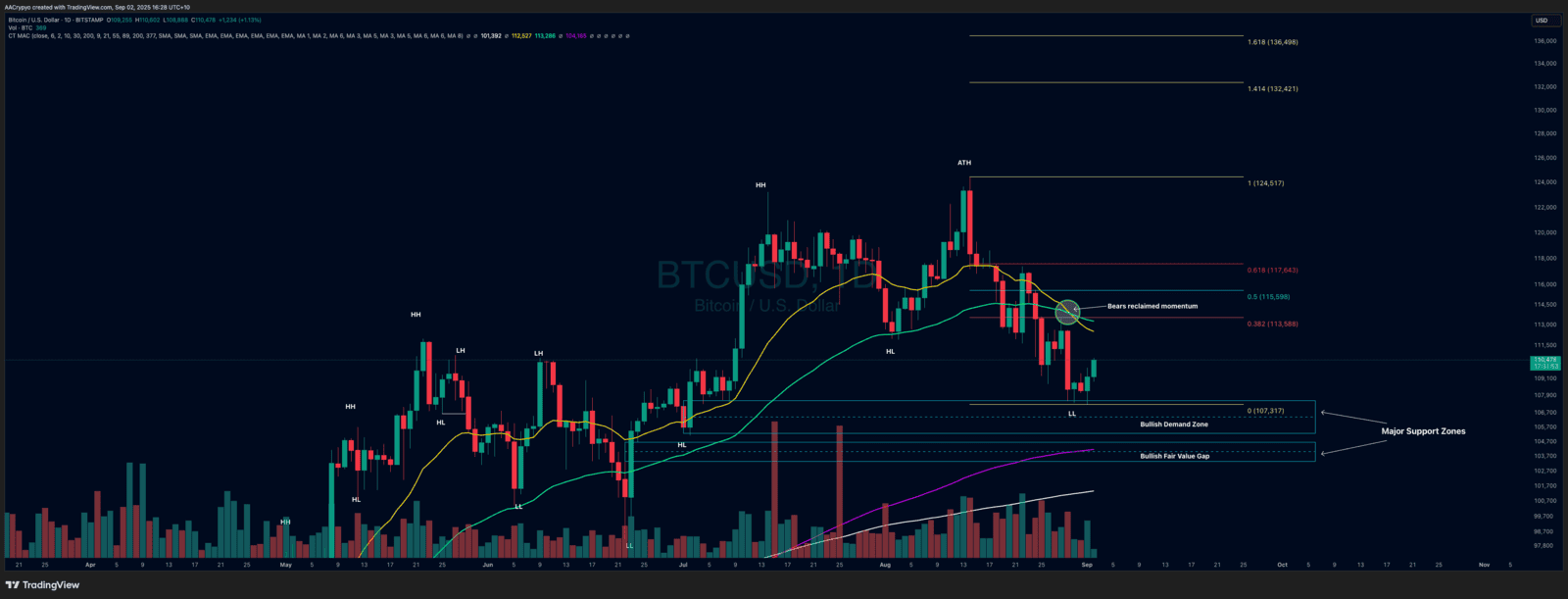

Bitcoin climbed to a new peak, ending the month nearly 7% higher at one point. But things turned fast. As sentiment flipped, the month closed red, down just under 7% from its high. It was a sharp reversal that caught many off guard.

Now we head into September, a month that has rarely been kind to Bitcoin. Historically, it is the worst-performing month on average for the asset, with a typical loss of 5.58% and nine of the last fourteen Septembers closing in the red. The trend is clear, and it is not just limited to crypto. September also has a poor track record for equities. Since 1926, the S&P 500 has averaged a return of minus 0.8% in September, and four of the last five years have followed that same negative pattern.

The current structure does not look great for Bitcoin, with August seeing both momentum and short-term control swing back to the bears. Entering what is statistically the most bearish month of the year only adds to the uncertainty. That said, the picture is not all bad. As shown in the chart, Bitcoin is now approaching a strong zone of technical support between $104K and $107K, with a deeper support band below that in the $102K to $103K region. If price continues lower and September plays out as history suggests, these levels should provide meaningful demand and could very well mark a short-term bottom.

These zones also align with what we would expect if Bitcoin were to post a typical September pullback of around 5%, which suggests any downside from here could be limited. From a structural perspective, this makes the coming weeks critical. If the support holds, the stage would be set for a potential rebound in October, which has historically been one of Bitcoin’s strongest months.

Breakout targets remain intact, with the shallow $130K region still acting as the key upside magnet. A move of nearly 20% would be required to reach those levels, but a steady September would set the scene for a strong fourth quarter, continuing the pattern of bullish momentum through October and beyond.

Macro could be the deciding factor. All eyes are on the 17 September interest rate decision, where markets are currently pricing in an 85% chance of a 25 bps cut. Powell’s dovish tone in August already boosted risk sentiment, and if a cut is confirmed, it could be the catalyst Bitcoin needs. One more inflation print is due before the meeting, and that could either confirm expectations or throw more confusion into the mix. If the Fed surprises with a hold, risk assets could face another leg lower.

Geopolitics also remains a wildcard. The potential meeting between Trump, Zelenskyy and Putin, expected in early September, could influence markets significantly. A move towards resolution in the Ukraine conflict would likely be seen as a major positive for risk assets.

So while history may not be on Bitcoin’s side heading into September, macro and technical support both offer reasons for cautious optimism. Bitcoin is vulnerable in the short term, but structurally it remains in the range of strong demand. The path forward depends on whether buyers step in here or wait for further confirmation. Either way, what happens in September could shape the rest of the cycle.

In the News:

In the News:

XRP Co-founder faces scrutiny for selling his tokens:

Controversy has been building around XRP co-founder Chris Larsen, as his wallet was recently linked to the sale or movement of 50 million XRP tokens, worth roughly $175 million around XRP's all-time high in July at $3.65. Around $140 million of that total ended up on exchanges, with the rest transferred to new wallets. The move has weighed heavily on XRP’s price action and added further pressure to an already bearish market backdrop. It has also reignited criticism around the project’s centralisation, with many investors frustrated by the perception that insiders are selling into retail demand. Any hopes of a bullish breakout have been temporarily halted.

Executive Order Opens Retirement Crypto Access in America:

In his push to position America as the global home of crypto, Trump signed another series of pro-crypto executive orders last month. The most impactful of these now allows Americans to purchase Bitcoin and other crypto assets within their 401(k) retirement plans, the US equivalent of Superannuation. This policy unlocks a major gateway, potentially giving over 90 million Americans direct exposure to the crypto market. It is a significant milestone for mainstream adoption and another tailwind for long-term demand.

Chainlink Partners with the US Department of Commerce:

Sticking with the broader theme of US-led crypto advancement, Chainlink has announced a partnership with the US Department of Commerce. The collaboration will bring key economic indicators, including real GDP and the PCE Price Index, on-chain to make the data immutable and publicly verifiable. This is a major step forward, not just for Chainlink but for the crypto space at large. By putting real-world economic data on the blockchain, the initiative signals growing institutional confidence in the technology and further legitimises the use case for decentralised data infrastructure beyond just Bitcoin.

Market Update:

Market Update:

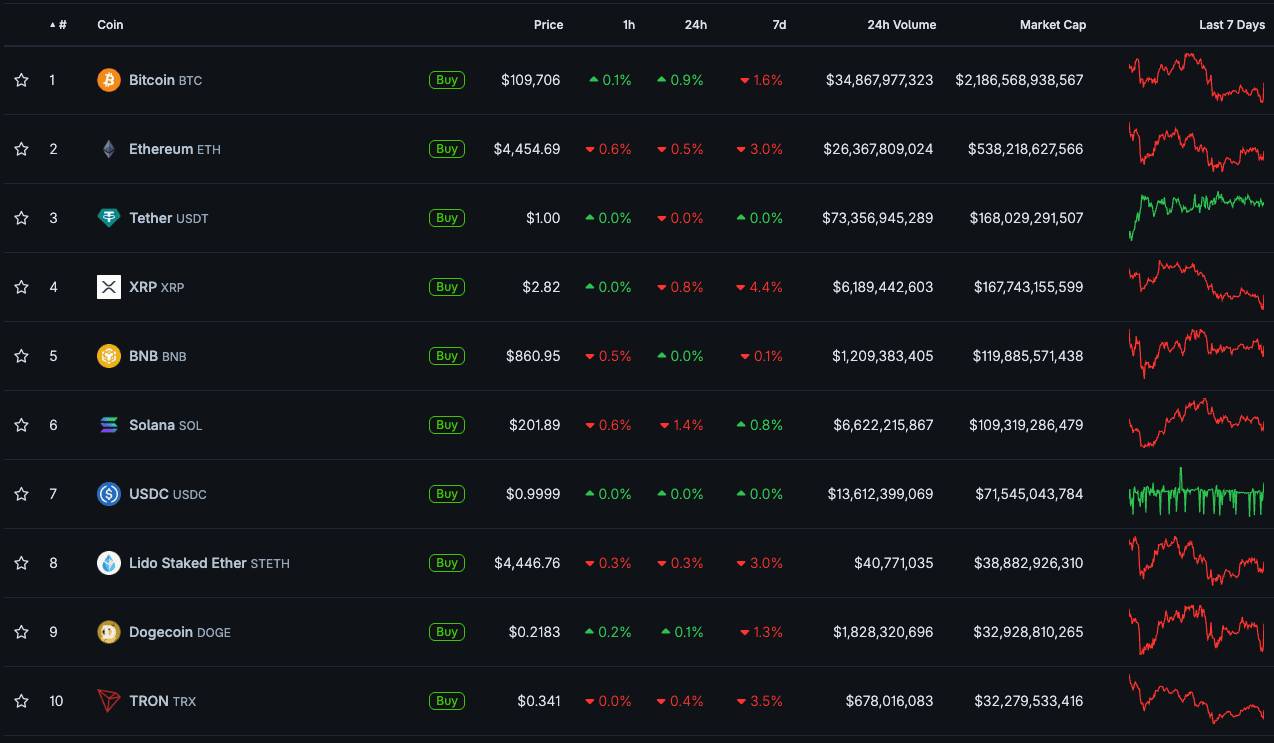

Here is the fast five of what you need to know about the market in August 2025:

- Bitcoin dropped 6.43% in August

- Ethereum gained 18.7%, continuing its strong run and setting a new all-time high

- Solana kept pace with ETH, finishing the month up 16.7%

- Chainlink led the majors, up 37.3% and climbing to the 13th largest crypto by market cap

- Total crypto market cap fell slightly by 0.56%

Video of the month:

Balaji Srinivasan: What Happens When Bitcoin Wins | Bitcoin Asia 2025

Education: Is There a Problem with Bitcoin Treasury Companies?

In the last cycle, we saw the collapse of hedge funds, trading firms and exchanges that were once considered too big to fail, until they were not. The unraveling of 3 Arrows Capital, Alameda Research and ultimately FTX dealt brutal blows to the market during the bear phase, sending Bitcoin and the broader crypto space even lower. A common thread ran through all of them: they were overleveraged and, in many cases, trading with borrowed or misused funds. As the bear market deepened and drawdowns accelerated, they fell like dominoes.

This cycle, the spotlight has shifted. Some critics now argue that Bitcoin treasury companies, which are firms holding large amounts of Bitcoin on their balance sheets, could become the FTX or 3AC of this era. The concern is that they are similarly vulnerable to collapse and could amplify downside pressure on Bitcoin’s price during periods of stress.

The Bitcoin treasury model has been led by Strategy (formerly MicroStrategy) CEO Michael Saylor. Under his leadership, the company has accumulated one of the largest corporate Bitcoin reserves by purchasing BTC directly and raising additional capital through convertible notes and equity offerings to buy more. In some cases, they have used debt financing, which increases the risk profile of the strategy. Other companies, such as Tesla and Block, have taken a different approach by using internal funds, but none have matched Strategy’s scale or aggressiveness. Recently, a handful of other Bitcoin-focused businesses have signalled similar intentions, taking inspiration from Saylor’s model.

It is not just Bitcoin seeing this trend emerge. Companies are beginning to adopt a similar strategy with other digital assets, including Ethereum and Solana. BitMine is currently the largest Ethereum treasury company, while Upexi holds the largest corporate position in Solana. As more companies join the trend and a broader range of assets become part of corporate treasuries, the risks begin to increase. With fewer safeguards, less liquidity and greater volatility across altcoins, the danger and likelihood of forced liquidations, poor risk management and eventual collapse become much higher. This raises systemic concerns not just for Bitcoin, but for the wider crypto market if this trend continues to accelerate without proper controls.

The core concern is leverage. Strategy has issued billions of dollars in debt to build its Bitcoin position. If a deep bear market drives prices sharply lower, the value of its holdings could fall to a point where the company struggles to service or refinance that debt. In a worst-case scenario, this could trigger forced Bitcoin sales, accelerating downside moves and shaking market confidence. While Strategy has already weathered one full bear cycle, the risk grows as the model is adopted by others. Critics warn it only takes one major failure to temporarily destabilise the market.

That said, even if a Bitcoin treasury company collapses and is forced to liquidate, it is crucial to remember that this risk sits with the company, not with Bitcoin itself. The network and asset remain fundamentally unchanged. Prices could fall in the short term, but Bitcoin’s core qualities such as scarcity, decentralisation and security are not affected by the actions of any single firm.

The analogy to the Global Financial Crisis is useful. In 2008, banks created risky debt instruments tied to mortgages. When the debt collapsed, markets crashed, but the houses themselves were still there. Similarly, if overleveraged crypto treasury companies fail, the Bitcoin, Ethereum or Solana they hold remains the same. The long-term value proposition does not disappear just because the wrong balance sheet strategy blew up.

Whether these companies thrive or collapse, Bitcoin remains Bitcoin. And now, so does Ethereum, Solana and any other asset chosen as a corporate store of value. For long-term investors, the noise around strategy, leverage and risk exposure should not distract from the core fundamentals. Volatility is part of the market, but the technology and value behind these assets persist regardless of how any one company chooses to manage its books.

Written by Alexandar Artis

Start Your Brokerage Account

If you enjoyed this Rake Review, feel free to open an account and gain access to more proprietary research and work with your very own dedicated crypto broker.

No Advice Warning

The information in this newsletter is general only. It should not be taken as constituting professional advice from the author - Stormrake PTY LTD.

Stormrake is not a financial adviser and does not provide financial product advice. You should consider seeking independent legal, financial, taxation or other advice to check how the information relates to your unique circumstances. Stormrake is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by this newsletter.

Disclaimer

All statements made in this newsletter are made in good faith and we believe they are accurate and reliable. Stormrake does not give any warranty as to the accuracy, reliability or completeness of information that is contained here, except insofar as any liability under statute cannot be excluded. Stormrake, its directors, employees and their representatives do not accept any liability for any error or omission in this newsletter or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information provided in this newsletter is owned by Stormrake. You may not alter or modify this information in any way, including the removal of this copyright notice.Copyright © 2022 Stormrake Pty Ltd, All rights reserved