When the Noise Became the Signal

When the Noise Became the Signal

When the Noise Became the Signal

June 2026 did not whisper. The world's biggest IPO sucked billions out of risk assets, Michael Saylor broke his four-year vow and sold Bitcoin for the first time, a new Fed Chair signalled rates may go higher before they go lower, and Bitcoin posted its worst monthly performance since the Luna/Terra collapse of 2022. For once, the noise and the signal were pointing in exactly the same direction.

The Biggest IPO Just Happened and Bitcoin Paid for It

Most people outside of finance have heard of SpaceX. Elon Musk's rocket company, responsible for sending astronauts to the International Space Station and building the Starlink satellite internet network, has for years been one of the most talked about private companies in the world. In June, it stopped being private. On June 12, SpaceX listed on the Nasdaq stock exchange under the ticker SPCX, raising $75 billion in what became the largest stock market debut in history. For context, the previous record was held by Saudi Aramco, which raised around $25 billion when it went public in 2019. SpaceX more than tripled it.

The excitement was enormous. Investor orders to buy shares exceeded $250 billion, roughly four times the amount SpaceX was actually selling, meaning the vast majority of people who tried to get in at the IPO price were turned away. The stock gained 19% on its first day and briefly pushed SpaceX's total value past $2 trillion. So what does any of this have to do with Bitcoin?

When a company raises $75 billion from investors, that money has to come from somewhere. Investors, both everyday people and large institutions, had to sell other things they owned to free up cash to buy SpaceX shares. And one of the assets people sold to raise that cash was Bitcoin. SpaceX effectively became a liquidity black hole, drawing risk capital that would otherwise have stayed in digital assets. This is called capital rotation, and it is one of the main reasons Bitcoin fell so heavily through June.

There is a twist worth knowing about. SpaceX's public filing revealed the company holds 18,712 Bitcoin on its balance sheet, worth approximately $1.29 billion. That makes SpaceX one of the largest corporate holders of Bitcoin in the world. The company that caused so much selling pressure in Bitcoin actually owns a significant amount of it. Every person who bought a SpaceX share in June now has indirect Bitcoin exposure, whether they realise it or not. And as SpaceX gets added to major stock market indices, thousands of index funds and pension funds that buy the stock will also be indirectly buying Bitcoin through SpaceX's treasury.

The deeper issue for Bitcoin this month was not just the money leaving, it was the attention leaving. SpaceX offered investors rockets, global internet, and artificial intelligence all in one stock. In a market where people chase whatever is exciting, Bitcoin simply cannot match the fresh story around SpaceX. For the better part of two years, Bitcoin was the most exciting trade in markets. That crown has been passed, at least for now, to AI stocks and space companies. SpaceX itself pulled back sharply after its debut, falling from an intraday high of $225 to around $153 by the end of the month, but by then the damage to Bitcoin sentiment had already been done.

The longer term picture is more positive, and there is a concrete reason for that. Capital rotation works in both directions. The same investors who sold Bitcoin to buy SpaceX shares will eventually look for the next opportunity, and Bitcoin, sitting at multi-month lows and testing its most historically significant long term support level, will be difficult to ignore. The IPO frenzy that hurt Bitcoin in June is temporary. The 18,712 Bitcoin now sitting on SpaceX's balance sheet, quietly embedded inside thousands of index funds and pension portfolios around the world, is permanent.

The Saylor Thesis Meets Gravity

If you have spent any time following Bitcoin over the past few years, you will have heard of Michael Saylor. He is the co-founder and executive chairman of a company called Strategy, formerly known as MicroStrategy, and he has built one of the most recognisable positions in crypto by doing one thing relentlessly: buying Bitcoin with every dollar he can get his hands on.

Strategy does not mine Bitcoin. It does not run an exchange. Its entire identity, since 2020, has been to accumulate as much Bitcoin as possible and hold it forever. To fund those purchases, the company has raised billions of dollars by issuing shares and debt products to investors. The pitch has always been simple: Bitcoin goes up over time, and owning a lot of it, acquired with borrowed and raised capital, produces extraordinary returns.

June tested that pitch.

On June 1, Strategy revealed it had sold 32 Bitcoin for approximately $2.5 million. It was the first time the company had sold any Bitcoin in four years. Now, 32 Bitcoin is not a lot. Strategy still held 843,706 coins after the sale, making it a fraction of a percent of their total position. But Saylor had said publicly, many times, that he would never sell. The moment he did, even a tiny amount, people started asking questions.

The reason for the sale was to pay a dividend to investors in one of Strategy's financial products, called STRC. This is essentially a type of investment that Strategy sells to raise cash, promising regular dividend payments in return. As Strategy has taken on more of these obligations, the bills have grown. Annual dividend payments have risen from around $300 million at the start of 2026 to $1.2 billion today, while the company's cash reserves have fallen 38% over the same period.

At the same time, Bitcoin's price has dropped well below what Strategy paid for most of its coins. The average price Strategy paid across its entire Bitcoin holding is around $75,500 per coin. With Bitcoin trading in the low $60,000s through much of June, the company is sitting on an unrealised loss of approximately $10.6 billion. That does not mean Strategy is in immediate trouble, unrealised losses are paper losses until you sell, but it does mean the financial pressure is real and growing.

Saylor's public response was to post on X: "Volatility tests every capital structure. Strategy remains focused on Bitcoin, disciplined capital allocation, credit quality, and long term value creation." Characteristically unfazed. His supporters point out that Strategy survived a worse situation in 2022, when Bitcoin fell below $16,000, and never had to sell. His critics point out that the company's obligations are significantly larger today than they were back then.

The honest answer is that nobody knows exactly how this plays out. If Bitcoin recovers strongly in the second half of 2026, Strategy's balance sheet improves quickly and the concerns fade. If Bitcoin stays flat or falls further, the pressure to sell coins to meet obligations becomes harder to ignore, and a forced sale from the world's largest corporate Bitcoin holder would create significant additional selling in the market.

There is one further development worth watching. Saylor has long positioned Strategy as a Bitcoin-only vehicle, but the financial pressure building on the balance sheet may force a rethink of that mandate. Speculation is growing that Strategy could begin diversifying its treasury into other hard assets, with gold the most likely candidate. If that happens, it would represent a significant shift in the Strategy story, and a tacit acknowledgement that a single-asset treasury model carries more risk than the narrative has historically admitted.

What June made clear is that the easy part of the Saylor trade is behind us. The thesis is not broken. Bitcoin has recovered from worse, and Strategy has survived deeper drawdowns than this one. But the risks are now visible in a way they were not twelve months ago, and visible risks have a habit of demanding attention before they resolve. The second half of 2026 will go a long way toward determining whether June was the moment the thesis was tested, or the moment it began to crack.

Price Performance: Breaking Down the Worst Month Since 2022

Price Performance: Breaking Down the Worst Month Since 2022

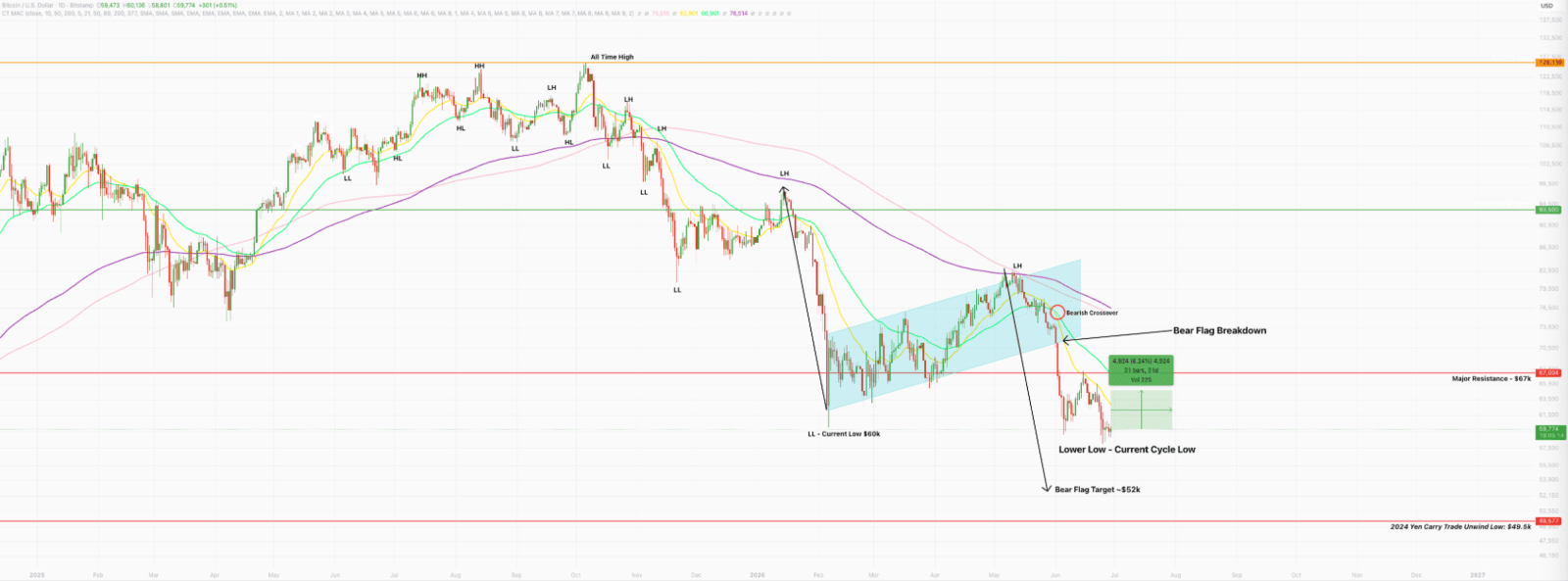

June broke what had been building for the majority of the year the classic bear market pattern known as the bear flag. This was the worst month for Bitcoin since June 2022, with Bitcoin losing nearly 19% from the open of the month to the close.

The month kicked off with a confirmed break of the bear flag, which triggered the next leg lower and the sustained bearish price action we saw throughout June. A major driver of sentiment this month was Michael Saylor and Strategy. When Strategy disclosed it had sold 32 Bitcoin the first sale in four years it shattered the narrative that Saylor was an unconditional, never sell accumulator. The market had priced Strategy as a permanent demand floor. The moment that assumption broke, confidence cracked with it, and the selling accelerated.

With the bears clearly in control, the bear flag pattern targets the mid to low $50,000 region as the next area of interest.

Despite June historically being one of Bitcoin's stronger months averaging an 8.24% return across nine green Junes in the last 16 years this year told a very different story, and one with a familiar feel.

June 2022 was also Bitcoin's worst month of that year, occurring in the aftermath of the Luna Terra collapse in May 2022, which was the first major blow of the previous bear market. This June drew extreme parallels to that period. The Luna collapse came seven months after Bitcoin's prior all time high. The current June drawdown has come eight months after the October 2025 all time high of $128,198. When the prior June collapse occurred, the market was closer to the end of the bear market than the beginning and that is what we are anticipating to be the case now.

We go much deeper into the outlook for the next few months in the Stormrake Q3 2026 Outlook, which you can find in the section below.

In the News

In the News

Stormrake Quarter 3 Outlook: The Final Washout

We have just released our Stormrake Quarter 3 2026 Outlook, titled 'The Final Washout'. The report covers the next three months of Bitcoin price action, where we think Bitcoin is headed, what is likely to drive it, and where we believe we currently sit in the broader market cycle. If you have been following Bitcoin through what has been a brutal June and want to understand what comes next, this is the place to start. You can find the full report in the section here. It is a must read for those looking to accumulate Bitcoin at a discount…

The US Iran War Is Winding Down And Oil Is Feeling It

Earlier this year, US and Israeli strikes on Iran in late February triggered the closure of the Strait of Hormuz, the narrow stretch of water between Iran and Oman through which roughly 20% of the world's oil supply passes. Brent crude surged from around $72 per barrel at the outset of the conflict to above $118 by late April, pushing inflation higher and forcing central banks to shelve any near term plans to cut interest rates. June brought meaningful relief. On June 18, the US and Iran signed an interim peace agreement, and oil prices fell sharply, with Brent dropping back toward $77 per barrel. By June 24, WTI had fallen below $70 per barrel for the first time since the war began. The ceasefire remains fragile and a permanent deal is far from done, but the direction of travel is positive. For Bitcoin, falling oil means falling inflation, which means the path to interest rate cuts reopens and cheaper money has historically been one of the most reliable tailwinds Bitcoin has ever had.

The New Fed Chair Just Made His First Call and It Was Not What Trump Wanted

Trump replaced Jerome Powell with Kevin Warsh in May 2026, widely expecting a more rate cut friendly Fed. On June 17, Warsh chaired his first meeting and voted unanimously to hold rates steady at 3.5% to 3.75%. The bigger story was what came alongside it. Nine of the 18 voting members now support a rate hike before the end of 2026, a sharp reversal from March, when not a single policymaker had pencilled one in. Warsh also scrapped the Fed's longstanding practice of forward guidance, removing any hint of where rates are heading next. Stocks fell immediately after the statement dropped. For Bitcoin, the message is simple: rate cuts historically one of the strongest tailwinds for crypto have been pushed even further down the road.

Market Update

Market Update

Here is the fast five of what you need to know about the market in June 2026:

- Bitcoin lost 19% in June.

- Ethereum fell by 21% in June.

- Hyperliquid created a new all time high at $76.70 but since retraced 20%.

- PAX Gold lost 12% in June.

- The total crypto market cap fell by 17%.

Video of the month

Sovereignty Brief Ep 1 -Who's holding your keys?

Bisher Khudeira and Michael Milmeister

Education: The 200 Week Moving Average

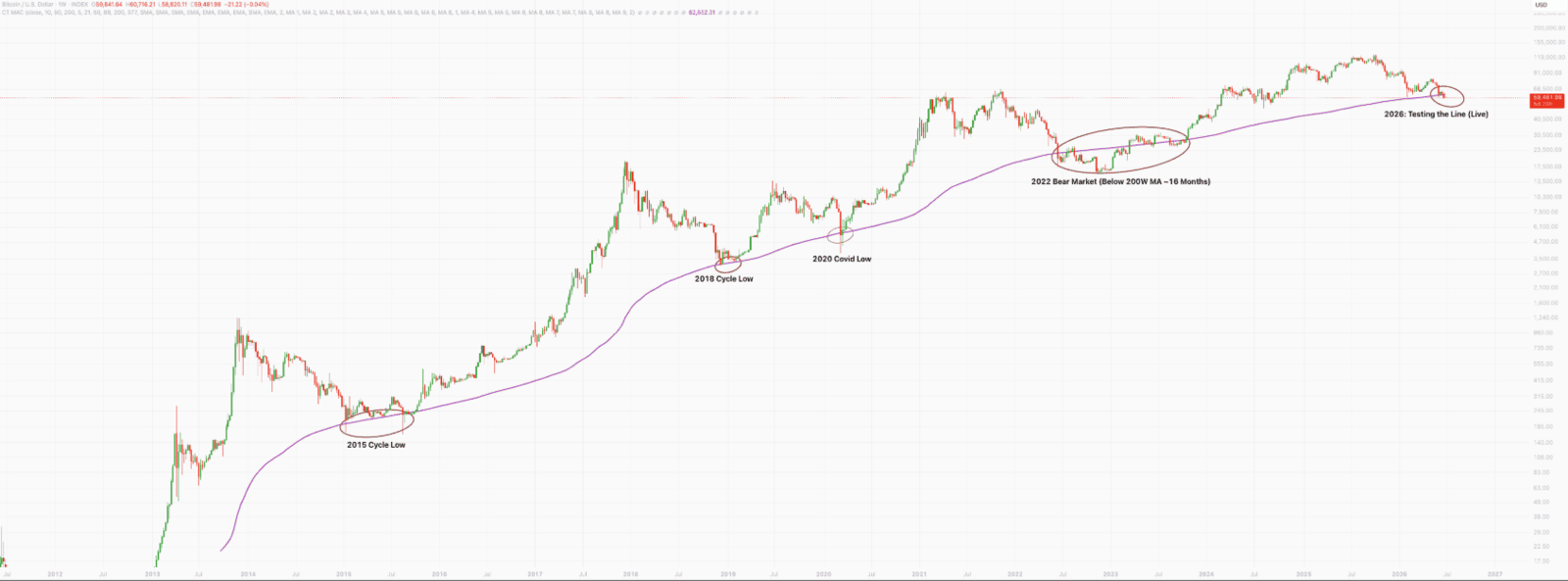

If you have been following Bitcoin through June, you will have seen a lot of commentary about something called the 200 week moving average. It has been mentioned constantly, and for good reason, Bitcoin spent much of this month right on top of it. So what is it, and why does everyone care so much?

Let's start simple. A moving average is just the average price of something over a set period of time. If you wanted to know Bitcoin's average price over the last ten days, you would add up the closing price from each of those days and divide by ten. That gives you a number, the average. Do the same calculation every day, updating it as new prices come in, and you get a line on a chart that smooths out the daily ups and downs and shows you the general direction things are heading.

The 200 week moving average does exactly that, but instead of using daily prices, it uses weekly prices, and instead of ten periods, it uses 200. That means it is calculating the average price of Bitcoin across the last 200 weeks, which works out to nearly four years of data in a single number.

Because it covers so much history, the line moves very slowly. It does not react to Bitcoin having a bad day, or even a bad month. It only really shifts when Bitcoin has been going in a particular direction for a long time. That makes it one of the most reliable tools for understanding where Bitcoin sits in its long term cycle, as opposed to its short term noise.

On June 4, Bitcoin tagged this line for the first time in this current cycle, with the moving average sitting near $62,600. That is why June felt significant to a lot of people watching the market. It was not just another bad month, it was Bitcoin arriving at the level that has historically signalled a floor.

The important thing to understand is that the 200 week moving average is not a guarantee. It is a pattern, not a rule. After breaching the line in June 2022, Bitcoin spent roughly 16 months below it before recovering. Touching it does not automatically mean the bottom is in. What it does mean is that Bitcoin has entered the kind of territory where, historically, patient long term buyers have been rewarded.

The cleanest signal to watch for is a weekly candle closing back above the line after touching it. That reclaim, price dipping to the average and then recovering above it, is what has marked the start of the next recovery in previous cycles.

For anyone who is relatively new to Bitcoin and feeling anxious watching the price sit in the high $50,000s and low $60,000s, the 200 week moving average is the context that matters most right now. It is not a reason to panic. If anything, it is the level where the most experienced long term holders in the market tend to get interested.

Written by Alexandar Artis

Start Your Brokerage Account

If you enjoyed this Rake Review, feel free to open an account and gain access to more proprietary research and work with your very own dedicated crypto broker.

No Advice Warning

The information in this newsletter is general only. It should not be taken as constituting professional advice from the author - Stormrake PTY LTD.

Stormrake is not a financial adviser and does not provide financial product advice. You should consider seeking independent legal, financial, taxation or other advice to check how the information relates to your unique circumstances. Stormrake is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by this newsletter.

Disclaimer

All statements made in this newsletter are made in good faith and we believe they are accurate and reliable. Stormrake does not give any warranty as to the accuracy, reliability or completeness of information that is contained here, except insofar as any liability under statute cannot be excluded. Stormrake, its directors, employees and their representatives do not accept any liability for any error or omission in this newsletter or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information provided in this newsletter is owned by Stormrake. You may not alter or modify this information in any way, including the removal of this copyright notice.Copyright © 2026 Stormrake Pty Ltd, All rights reserved