Bitcoin’s True Purpose

Bitcoin’s True Purpose

Bitcoin’s True Purpose

Bitcoin is not the next safe haven but the next global reserve currency. As fiat systems crack and liquidity returns, Bitcoin’s true role is emerging. This is not a repeat of past cycles but a structural reset. Still undervalued, still early.

Bitcoin Is Not a Safe Haven but Something Bigger

For a long time, people positioned themselves in Bitcoin as a modern version of a classical safe haven asset, comparable to gold or silver. While the price correlation has not held for over half a decade, the narrative persisted. But the last 12 months, and particularly January, have thrown a clear spotlight on the negative correlation between the two.

There is no debate that gold, and by extension silver, remains the dominant safe haven. With over 5,000 years of proven history, gold has long served as a reliable store of wealth. Bitcoin was dubbed ‘Digital Gold’ early on, sharing traits like finite supply, resistance to replication, and protection against fiat currency devaluation. But beyond these shared characteristics, the assets behave quite differently and that distinction benefits both.

Gold thrives in risk off environments, a trend made clear over the past year. It has performed well alongside silver, which has arguably been the standout asset of the past 12 months. Despite the similarities in branding, Bitcoin’s purpose is not to replace gold as a safe haven. Nor is it purely a risk on asset, although it tends to outperform when liquidity flows freely through the economy.

Bitcoin was originally built to exchange value peer to peer, without the need for third parties or centralised intermediaries. It served that role early on, particularly during the Silk Road era and through small-scale peer to peer transactions. Over time, its volatile price action and cyclical behaviour have aligned it more closely with risk assets, leading to a perception of it as a speculative vehicle, a ‘number go up’ asset.

As the space drifted from Bitcoin’s original intent, the past month has served as a reminder of its core purpose. This time, though, the shift comes with global awareness and real infrastructure backing the transition.

The US Government Are the Architects of Their Own Demise

It is not every day you watch the world’s biggest currency unravel in plain sight, and yet that is exactly what is happening with the US dollar. Orchestrated by the US Government itself.

January was one of the busiest months in recent memory, not for Bitcoin’s price action but for macro events. While Bitcoin has not yet made a significant move, under the surface new opportunities are emerging, triggered largely by the actions of the US Government.

Headlines were dominated by controversy over US involvement in Venezuela, a heated tariff standoff involving Greenland that eventually ended in a deal, and yet another looming government shutdown over ICE funding. While we will not dive into those in this note, two specific developments carry far more weight and could reshape not just Bitcoin’s future, but the global financial system as a whole.

We have been covering the deterioration in the Japanese economy and the yen for several months, and it now looks like the long anticipated intervention has arrived. The US is selling dollars to buy yen in an attempt to stabilise Japan’s currency. But this move has broader consequences. By actively weakening the dollar, the US is eroding its own citizens’ purchasing power. And because the US dollar is still the global reserve currency, this erosion affects nearly everyone, whether they realise it or not.

To dive deeper into the BOJ's role and how yen intervention may impact Bitcoin, read our full breakdown:Bitcoin, BOJ Yields, and the Yen: The Next Financial Tug-of-War

As a result, most assets priced in USD, which is nearly everything, appear to be rising. But if everything is increasing against the dollar, the key question becomes: are these assets actually gaining value, or is the dollar simply losing it?

Markets are already pricing in the intervention. The DXY has begun to decline against all major currencies including the yen, and traders are preparing for the official confirmation. This move may accelerate volatility, particularly in the yen carry trade. Institutions that borrowed yen using USD may now need to sell risk on assets to unwind their positions as the yen strengthens. That could bring temporary downside pressure, but at the same time, Bitcoin and other USD denominated assets are likely to benefit from continued dollar weakness.

But price action is not the core issue here. The real concern is the structural weakness of fiat currencies, and more critically, the vulnerability of the global reserve currency itself. This is not the first time the US has deliberately devalued the dollar to support a foreign currency. Each time it happens, it chips away at the dollar’s credibility and damages trust. It punishes the public, hollows out purchasing power, and nudges both individuals and institutions toward alternative stores of value. No matter which nation holds the reserve currency title, if the system is fiat based, it is inherently unsustainable. History is full of failed fiat regimes. This latest intervention is simply another signal that the US dollar is no longer fit to serve as the global benchmark. And that is exactly where Bitcoin enters the conversation.

The definition of insanity is doing the same thing repeatedly and expecting different results. So no, a new fiat global reserve currency is extremely unlikely. Gold and silver have both played that role before, but each comes with limitations. Bitcoin offers a modern solution. It is not controlled by any single party, it cannot be diluted or manipulated, and it shares many of gold’s advantages while removing the pain points. It is highly divisible, borderless, has no physical storage requirements, and can be transacted and settled within minutes.

Bitcoin is the only real candidate for the next global reserve currency. Investors should not view it as a safe haven replacement or a trade for number go up. They should understand and embrace its core purpose. That purpose is only fulfilled once it becomes the global reserve and unit of account. Every move in price between now and then is simply the side effect of that long term trajectory.

The US Is Not on a Sustainable Path

The US Is Not on a Sustainable Path

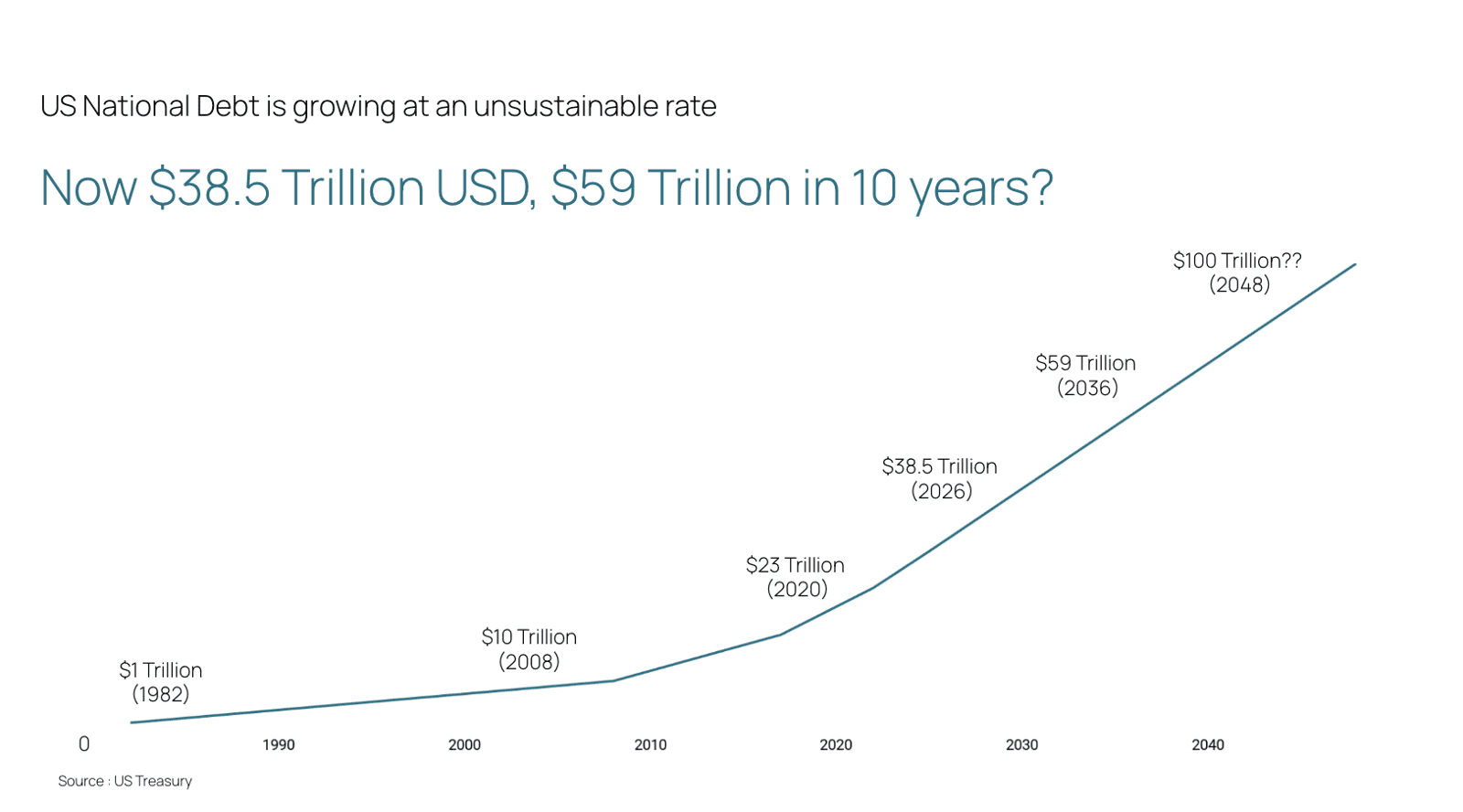

The US Government is not only responsible for the demise of the dollar through monetary intervention, it is also undermining its own economy. US national debt has surged to $38.5 trillion, with over a third of it needing to be refinanced this year alone. This was a central point in our Stormrake 2026 thesis and one of the most bullish macro factors for Bitcoin.

Even Jerome Powell, Chairman of the Federal Reserve, has admitted that the level of US debt is not unsustainable, but the path is unsustainable. Back in 2020, the national debt stood at $23 trillion. In just six years, that figure has increased by more than 50 percent. This has dramatically devalued the dollar and fuelled inflation through unchecked money printing. The strategy has been to kick the can down the road, but time is running out. Some forecasts put total US debt at $59 trillion within a decade, and potentially at $100 trillion by 2048 if this trend continues.

The issue is not just the total debt. It is also the debt to GDP ratio, which now exceeds 120 percent. This figure measures how much debt a country holds relative to its economic output, and it is widely used to assess fiscal sustainability. In general, the lower the better. Once a country crosses the 120 percent threshold, history suggests there is often no return. The result is either hyperinflation or the end of reserve currency status.

Weimar Germany, Venezuela and Argentina are all examples of hyperinflation following unsustainable debt to GDP levels. But the last time a global reserve currency faced this dilemma was post World War II Britain. The UK’s debt to GDP ratio hit 250 percent. While it avoided hyperinflation, the pound sterling quickly lost its global reserve status. It was replaced by the US dollar.

History may not repeat, but it often rhymes. Based on the current trajectory, the US dollar is likely to suffer a similar fate. Whether it ends in hyperinflation or a changing of the guard, both outcomes point to one thing. A bullish future for Bitcoin.

2025 to 2026: A Replay of 2021 to 2022?

2025 to 2026: A Replay of 2021 to 2022?

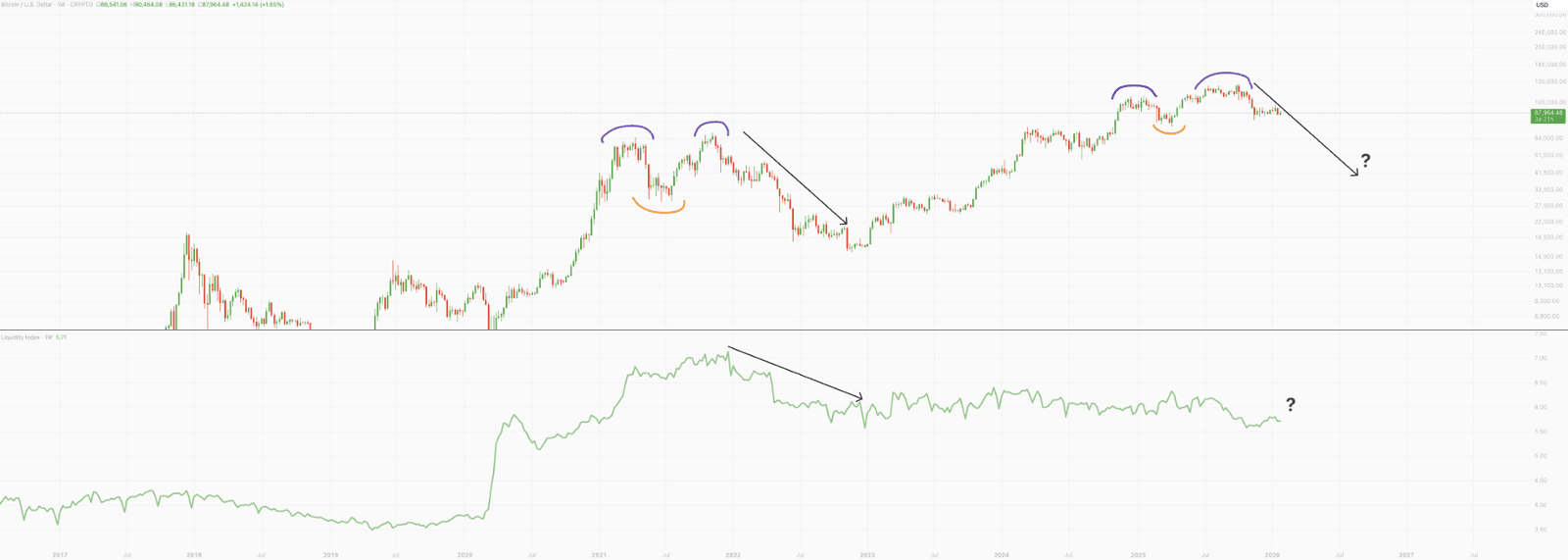

One of the key narratives throughout January was whether this market is simply repeating the same cycle we saw four years ago. From a technical perspective and in terms of market structure, the similarities are undeniable. But the macro backdrop is very different.

The chart above shows Bitcoin price action in the top panel and the US liquidity index in the bottom panel. There is no denying that the pattern between 2021 and 2022 and what we are seeing in 2025 and 2026 looks remarkably similar. In both cases we saw an all time high, followed by a deep correction, and then another marginal all time high. Back in 2021, the peak was followed by a nearly 80 percent drawdown during the bear market. While we have not yet seen a correction of that magnitude this time, many are calling for a repeat. But there is one crucial macro difference, liquidity.

Bitcoin thrives in high liquidity environments, and this time the liquidity dynamics are the opposite of what they were in 2022. Back then, the US Federal Reserve delivered one of the fastest rate hike cycles in history, drained liquidity by rolling over its balance sheet, and avoided new Treasury purchases. In short, they were pulling dollars out of the system.

In 2026, we are now seeing interest rate cuts, the Federal Reserve is once again buying US Treasuries, and liquidity is flowing back into the system. Quantitative tightening has ended, and the market is starting to price in the return of quantitative easing.

At this moment, liquidity appears to be basing, if not already rising. That matters. Bitcoin performs best in environments where liquidity is expanding. So when people argue that this cycle is simply repeating the last, they are often ignoring the single most important driver behind Bitcoin’s price action.

This does not mean Bitcoin cannot correct lower in the short term. But if liquidity continues to increase, it becomes extremely unlikely that Bitcoin will follow the same path it did in 2022.

In the News

In the News

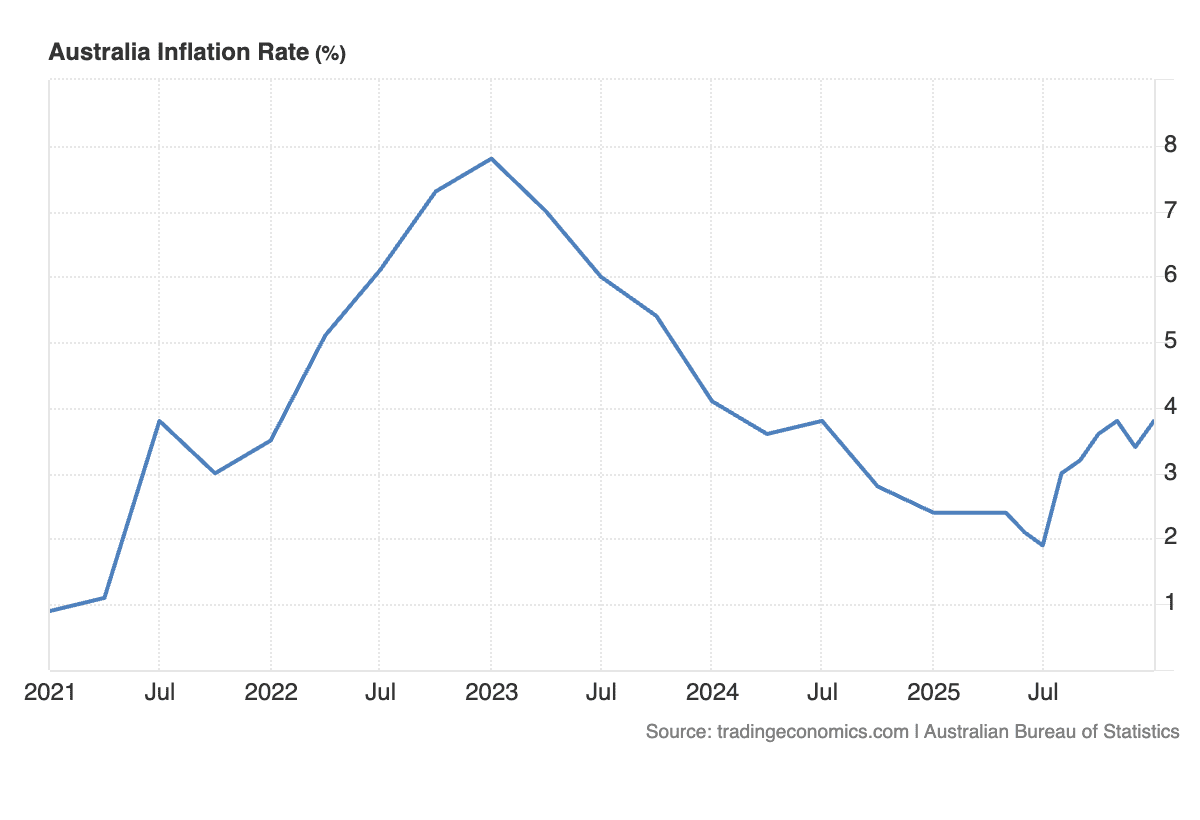

Australian Inflation Surprises to the Upside

The Reserve Bank of Australia targets 2 to 3% inflation, but the latest data shows price growth rising faster than expected. December’s CPI came in at 3.4% year on year, with forecasts for this release at 3.5% and a 0.7% month on month rise. When the data landed on 28 January, CPI had jumped to 3.8% year on year and 1% month on month, well above estimates. With an RBA rate decision due early next month, market expectations have flipped. There is now a 79% chance of a rate hike, compared to just one week ago when no change was priced in at 89%.

Trump Nominates Kevin Warsh as Fed Chair

President Trump has nominated Kevin Warsh as the next chairman of the US Federal Reserve. Warsh, who is seen as traditionally hawkish on monetary policy, triggered selling pressure across gold, silver and Bitcoin when the announcement was made. However, one key distinction is that Warsh has expressed pro Bitcoin views over the years in interviews, calling it an innovation that challenges fiat mismanagement. His appointment adds to what is now a fully pro Bitcoin administration under Trump, which can only support Bitcoin in the long term.

Warsh is set to replace Jerome Powell when his term ends in May. There are two Federal Reserve meetings before then, but markets widely expect rates to remain on hold at both.

Gold and Silver Snap Their Parabolic Run With a Sharp Correction

Just days after crypto exchanges began listing futures markets for gold and silver, with users leveraging altcoins to chase exposure, both metals saw brutal corrections. While the crypto derivatives were not the direct cause, their sudden appearance marked a clear sign that the top was near.

Silver posted its worst single day performance in 40 years, falling nearly 30% in one session. Gold also dropped sharply, correcting by 10% in a single day. The parabolic move unwound quickly, triggering major drawdowns and leaving late entrants and retail traders caught on the wrong side of the trade.

Market Update

Market Update

Here is the fast five of what you need to know about the market in January 2025:

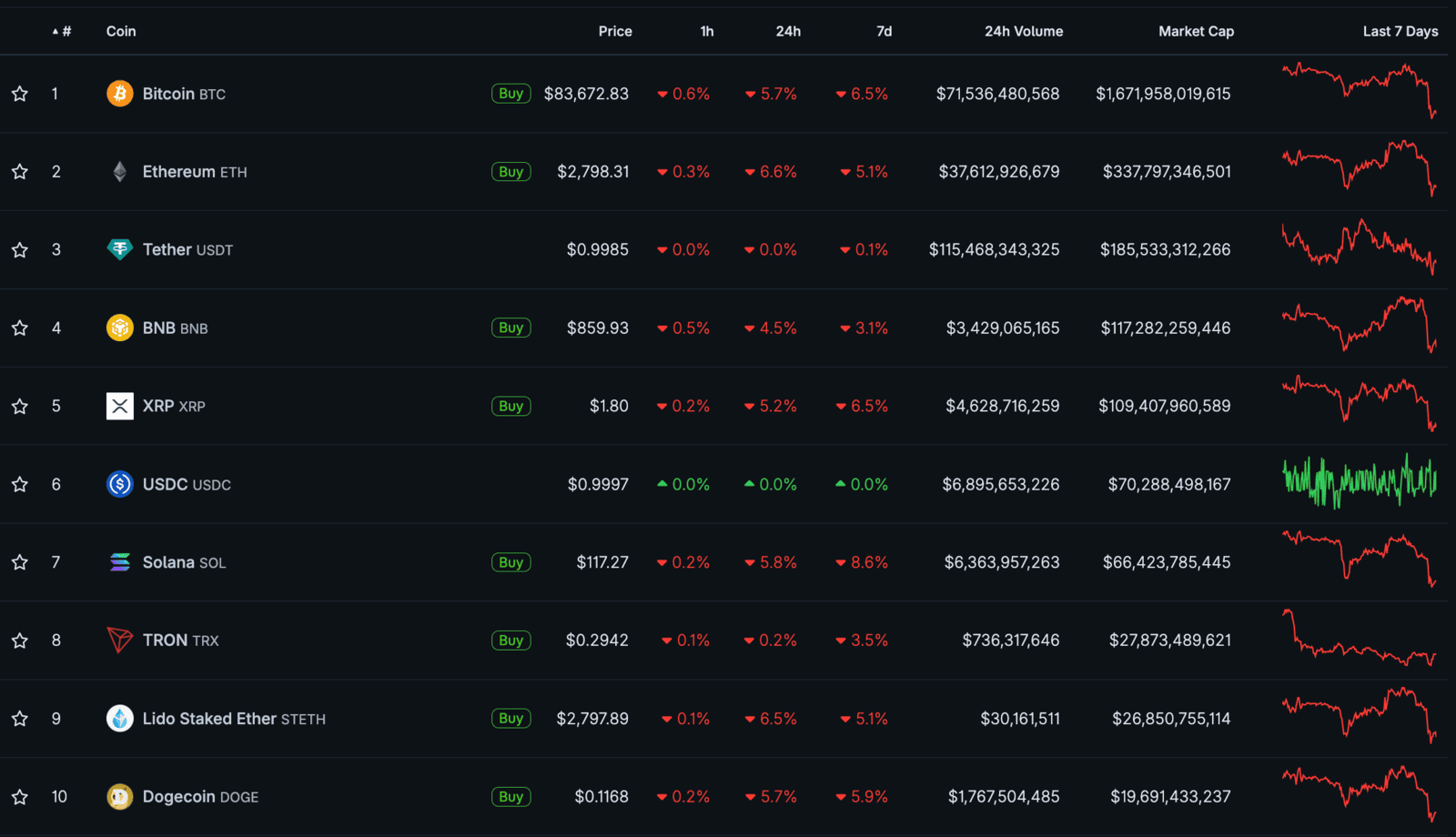

- Bitcoin fell 4.3% in January

- Ethereum fell 5.5% in January

- BNB flipped XRP to climb into 4th spot

- PAXG was a standout, up 25% when the majority of the market was red

- The total crypto market cap fell by 3.7%

Video of the month

Could Bitcoin Fall to $60,000 in 2026 and What Should Investors Do?

Stay Ahead With the Stormrake Morning Note

For more frequent Bitcoin market insights, macro catalysts, and technical deep dives, subscribe to our daily Stormrake Morning Note.

Concise, insightful, and built to keep you informed about everything that is going on...

SUBSCRIBE HERE

SUBSCRIBE HERE

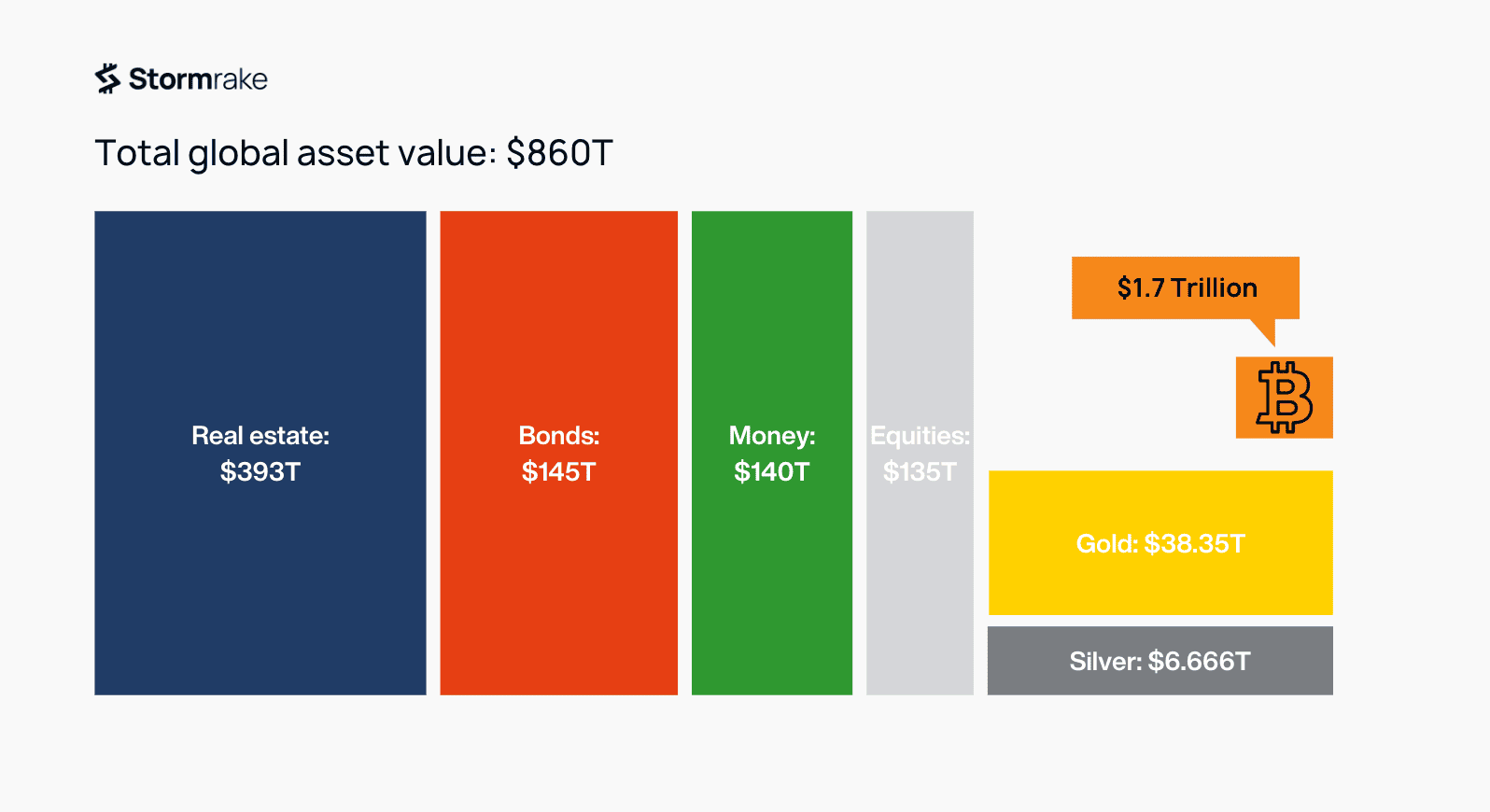

Education: Understanding Global Macro Asset Classes

Many readers will recognise the visual above. It breaks down major global asset classes and shows the real size of each in comparison. Global real estate dominates the chart, followed by bonds, money markets and equities. Gold and silver, despite recent rallies, remain much smaller than equities. But what stands out most is Bitcoin's position.

This graphic is a reminder that asset valuations should be compared by market cap, not by price. Bitcoin trading at $90,000 and gold at $5,500 does not mean Bitcoin is more valuable. Market cap is the metric that matters.

Smaller market caps tend to come with more volatility. It takes far less capital to move a smaller market than a larger one. For context, gold gained $500 per ounce in just 72 hours, moving from $5,000 to $5,500. In that same window, its market cap increased by $3.5 trillion — more than double Bitcoin’s entire market cap, and it happened in under three days.

Bitcoin currently has a market cap of $1.7 trillion. That alone shows how early we still are. If Bitcoin were to reach silver’s current market cap of $6.666 trillion, it would imply a Bitcoin price of roughly $350,000. Bitcoin’s all time high in October 2025 saw a $2.5 trillion market cap with price peaking at $126,000.

A $6.666 trillion market cap is conservative if Bitcoin continues on its adoption curve and fulfills its long term purpose. Michael Saylor, Bitcoin’s most vocal bull, has projected a $441 trillion market cap by 2046 — absorbing a large share of gold’s monetary role — with a price target of $21 million per coin. While that figure seems outrageous to many, surpassing silver and matching gold’s market cap is not far fetched.

This also does not mean gold or silver have to fall for Bitcoin to rise. All three assets can rally together, with Bitcoin simply outperforming. At gold’s current market cap, Bitcoin would be priced at around $2 million.

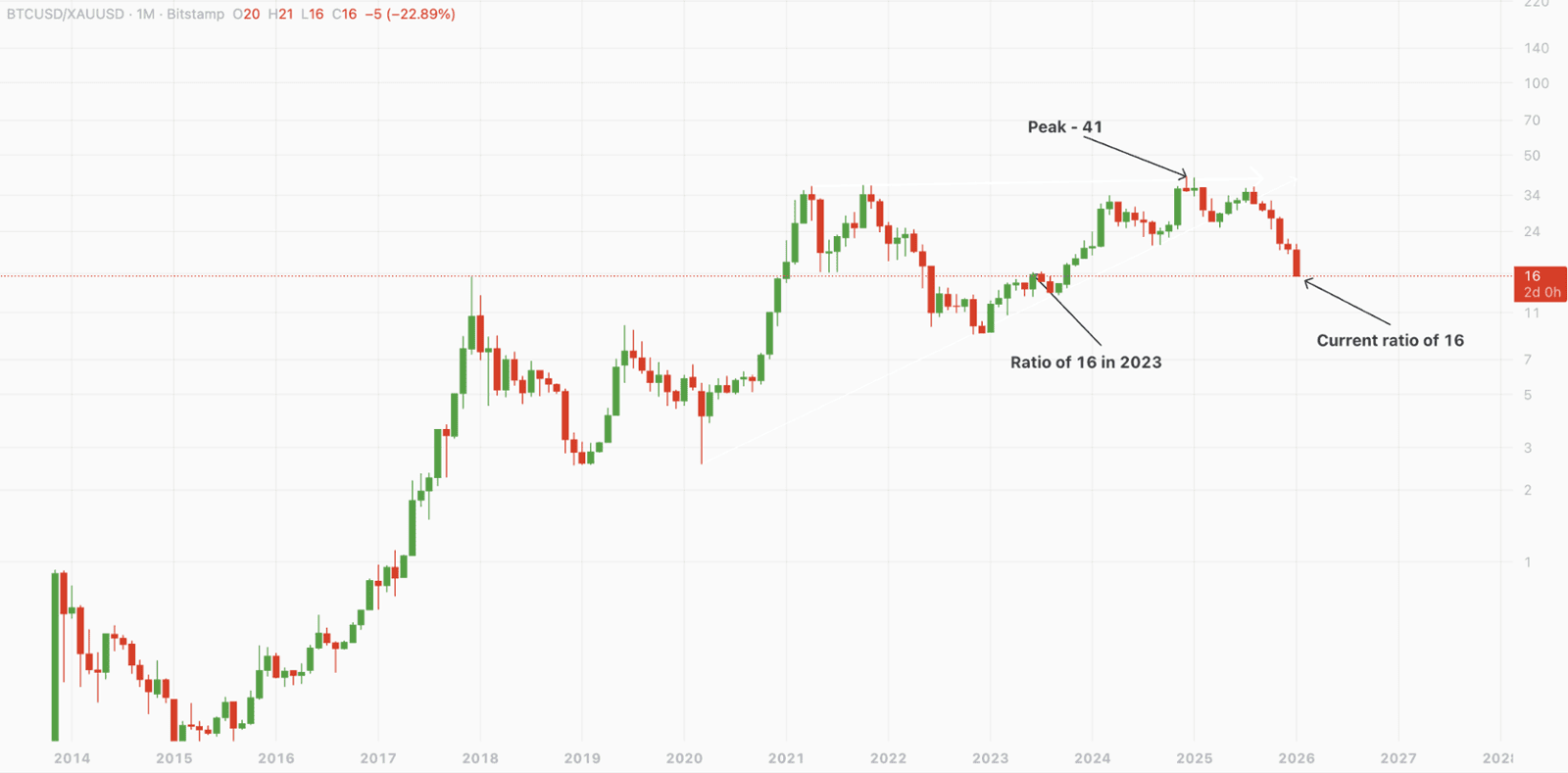

To dig deeper into the comparison, let’s look at the Bitcoin to gold ratio.

The chart above shows how many ounces of gold can be bought with one Bitcoin. Right now, the ratio sits at 16, meaning one Bitcoin can purchase 16 ounces of gold. This comes with Bitcoin at $88,000 in a corrective period and gold at record highs around $5,500. The ratio peaked at 41 in late 2024. Since then, gold has outperformed Bitcoin by 60%, pulling the ratio back to levels not seen since August 2023.

So what does this mean?

It is a strong signal of undervaluation. The last time the ratio was this low, Bitcoin was trading between $25,000 and $30,000. Despite now sitting at $88,000, Bitcoin has underperformed against gold, returning to relative levels from years ago. That divergence makes this a clear buying opportunity for those looking to rotate back into Bitcoin. When the ratio resets higher, Bitcoin typically sees strong outperformance in the following months.

You're still early. Out of all the major asset classes, Bitcoin makes up just 0.2% of global value. Regardless of its nominal price, as Bitcoin’s market cap grows and it continues gaining market share against other global assets, the dollar figure will follow.

Written by Alexandar Artis

Start Your Brokerage Account

If you enjoyed this Rake Review, feel free to open an account and gain access to more proprietary research and work with your very own dedicated crypto broker.

No Advice Warning

The information in this newsletter is general only. It should not be taken as constituting professional advice from the author - Stormrake PTY LTD.

Stormrake is not a financial adviser and does not provide financial product advice. You should consider seeking independent legal, financial, taxation or other advice to check how the information relates to your unique circumstances. Stormrake is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by this newsletter.

Disclaimer

All statements made in this newsletter are made in good faith and we believe they are accurate and reliable. Stormrake does not give any warranty as to the accuracy, reliability or completeness of information that is contained here, except insofar as any liability under statute cannot be excluded. Stormrake, its directors, employees and their representatives do not accept any liability for any error or omission in this newsletter or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information provided in this newsletter is owned by Stormrake. You may not alter or modify this information in any way, including the removal of this copyright notice.Copyright © 2026 Stormrake Pty Ltd, All rights reserved