The Calm Before Q4’s Big Move

The Calm Before Q4’s Big Move

The Calm Before Q4’s Big Move

September has wrapped up. Bitcoin fought through historical stigmas, liquidations, and manipulation to close green. A new narrative dominated headlines and shook the space, while fresh signs of adoption continue to emerge. Through it all, Bitcoin held firm and September has now set the stage for October.

Driven by Expectations and Historical Patterns

We’ve just wrapped up Bitcoin’s historically worst month of the year, September. And much like the rest of 2025 so far, it was mixed. Both bulls and bears had their moments in the sun, but by the end of it, Bitcoin once again fought its way back on top.

The dominant narrative this year has been interest rates. Off the back of 2024, where we saw a full 100bps cut between September and December, markets began pricing in the potential for up to five rate cuts in 2025. That idea fuelled rallies across all risk-on assets. Fast forward to today, and with only two decisions left on the calendar, it’s clear there won’t be five cuts. But despite that, markets have still pushed to new all-time highs across multiple sectors.

After months of pressure, including criticism from the US President, Powell and the Federal Reserve finally made the call to cut rates. While the actual cut didn’t move price much on the day, the signal was loud and clear. The door is now open. We already saw a preview of this at Jackson Hole in August, where Powell hinted at a shift in policy for the upcoming September meeting. Markets responded with strength. With two more cuts still expected, the final quarter of the year could carry serious potential for further all-time highs and broad risk-on strength.

When it comes to price manipulation, Bitcoin is no stranger. Large exchanges and institutions regularly push price in a certain direction to trigger liquidations on leveraged positions. This is often done to collect additional fees or to drive price lower for better entries before a reversal. These moves aren’t sustainable because they’re not driven by genuine buying or selling interest. Instead, they’re often triggered by large players temporarily moving price to force liquidations, not to establish long-term positions.

Over the past year, we’ve seen several brutal liquidation days, mostly targeting overleveraged longs. While 2025 hasn’t seen as many as previous years, December 2024 still had multiple days with over $1 billion in liquidations. The largest came in at $1.8 billion, which triggered a 6% drop in Bitcoin. Fast forward to this September, we saw two more days in the same week with over $1 billion wiped from the market. The biggest was on the 22nd, when $1.7 billion was liquidated. But this time, the reaction was far more muted. Bitcoin dropped less than 2.5%.

To put that into context, the FTX collapse in 2022 triggered $1.5 billion in liquidations over six days, and Bitcoin dropped nearly 30%. That comparison highlights how far the market has matured. Institutional adoption and deeper liquidity mean that multi-billion dollar liquidation events now have a reduced impact on price.

As Bitcoin continues to grow, these events will likely have less and less influence on daily price action. But manipulation will always remain. The main takeaway is that these liquidation pullbacks continue to present prime opportunities to accumulate. Because no matter how wild things get in the short term, Bitcoin’s long-term direction hasn’t changed — it still moves up and to the right.

Bull Markets Are Fuelled by Narratives

Bull Markets Are Fuelled by Narratives

Bull markets are driven by narratives, whether in crypto or traditional markets. These narratives can be sector-focused or broad market-wide themes, but they all drive price action. Investors chase the hottest stories, and that chase fuels momentum and outsized performance. Once one narrative fades, another takes its place. It’s a cycle within a cycle.

Some of the strongest bull markets have been powered by genuine macro narratives. In 2021, we saw the post-pandemic stimulus era take hold. Government handouts and free-flowing capital didn’t just pump stock and crypto markets — they sent everything into bull mode. The current bull run, while slightly different, is no less powerful. Some argue it’s a tech and AI-driven rally in traditional markets, while others point to Bitcoin’s breakout being led by institutional adoption. Both are true, but the foundation of this entire move is simple: the money printer is back, inflation remains sticky, and investors are looking for alternative vehicles to generate returns and preserve wealth.

The bull run out of the pandemic and the current one share a common core — easy money and systemic macro pressure. As Bitcoin matures, its correlation with these broader macro themes continues to strengthen.

Crypto has had its own defining cycles too. In 2013, Bitcoin’s “digital gold” and “safe haven” status took off during the Cyprus banking crisis. Google searches spiked 10x, and Bitcoin rallied 5x on the back of it. In 2017, the ICO craze drove altcoins and Ethereum to dizzying heights.

This current crypto bull run has had no shortage of narratives either. It started with the Bitcoin ETF rumours and eventual approvals, which helped drive further institutional adoption. Then the narrative shifted to inflation and the macro setup. From there, sector-specific rallies began to break out. Solana pushed to new highs off the back of the memecoin casino in January. AI-focused projects like FET (now ASI) and Bittensor (TAO) caught strong bids. Ethereum and its broader ecosystem also saw renewed attention as institutions began building and adopting ETH-native infrastructure.

And then came a new narrative.

And then came a new narrative.

The headlines in September were dominated by one theme — Decentralised Exchanges (DEXes). Earlier in the year, Hyperliquid launched its token and quickly made waves, establishing itself as a top 20 crypto by market cap and capturing a large share of onchain DEX users. But September saw a shift. Aster, a new DEX built on Binance Smart Chain and backed by major players in the space, exploded onto the scene.

The result was a major user migration from Hyperliquid to Aster as the hype built. ASTER rallied from under $0.02 to over $2.40 in under two weeks, while HYPE fell over 30% after setting a new all-time high earlier in the month. Aster’s explosive launch also had a ripple effect on BNB, the native token of Binance Smart Chain, which hit an all-time high off the back of increased onchain activity.

The question now is whether Aster can hold the momentum. Hyperliquid has already established itself as a long-term player. If Aster can maintain its user base and liquidity, it could shape up to be the one-two punch in the DEX space.

This was a clear sector-driven narrative within the broader market. Looking ahead, the next narrative is already forming — interest rate cuts and the historical strength of Q4, which has consistently been the most bullish quarter for risk-on assets.

September Holds Strong, Uptober Now in Focus

September Holds Strong, Uptober Now in Focus

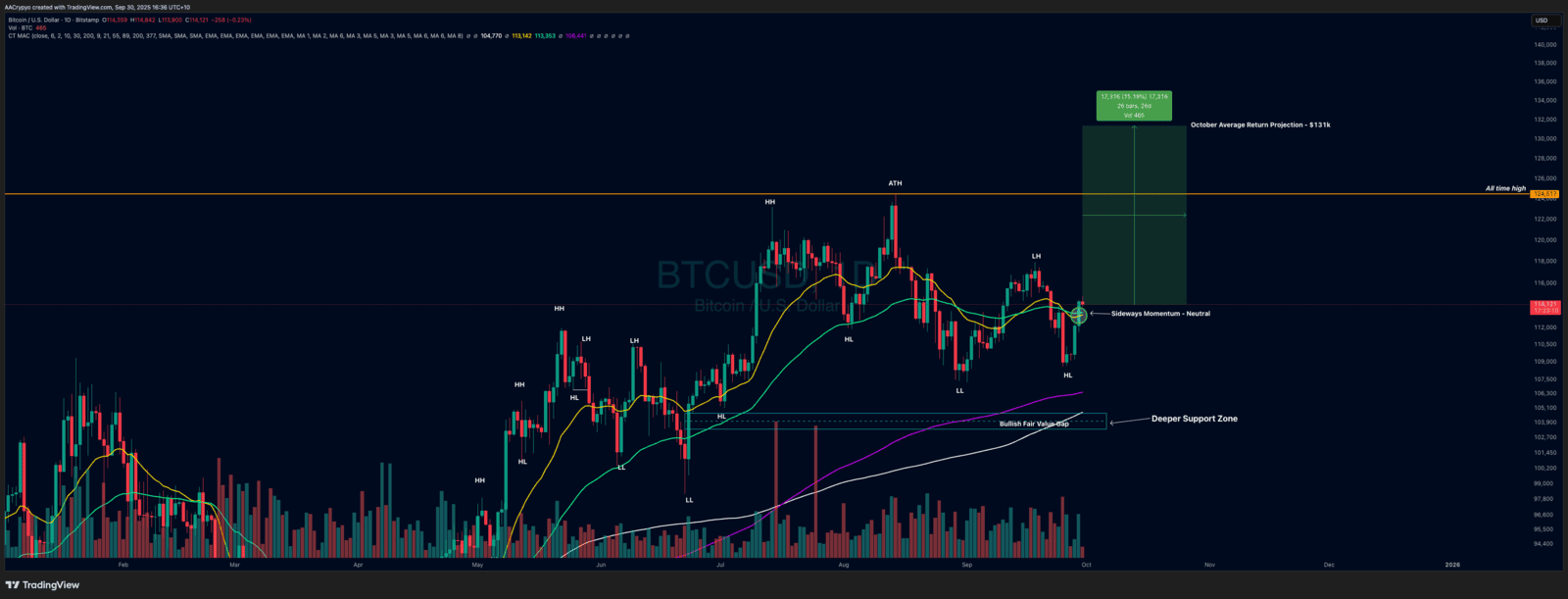

Heading into September, Bitcoin was under pressure. Bears were out in force, calling for the end of the bull market, and history was on their side. September is Bitcoin’s worst-performing month on record. Most would have bet on a red monthly close. But once again, Bitcoin proved the doubters wrong, closing the month green and up 5%, despite late-month pressure from liquidations and expiring options.

Even with that bearish backdrop and sentiment, Bitcoin held its ground. Now it is preparing for the most bullish period of the year — Uptober and the fourth quarter. October ranks as Bitcoin’s fourth-best month by average return at 15.2%, but it stands out as the most commonly green month, with only four red Octobers since 2011.

In addition to seasonality, October is expected to bring the penultimate rate cut of the year. As of writing, there is a 90% chance of a 25 bps cut. While the market may already be anticipating it, the fact that it is happening adds another bullish catalyst to what is shaping up to be a strong month for risk-on assets.

Looking at the current technical picture, Bitcoin is closing out September in a relatively neutral stance. Momentum is sideways, and structure is in no man’s land, with a lower high and a higher low forming the present range. This setup gives both bulls and bears a clean shot at taking control in October. However, historical performance and macro catalysts suggest the bulls are more likely to come out on top. If Bitcoin simply matches its average return for October, price would break to a new all-time high above $131,000.

Although September may have felt like a flat or slightly bearish month, the reality is that it was quietly bullish. And now, as we enter the most favourable time of the year, the opportunity is still there. Bitcoin is trading at a near 10% discount from its all-time high, and many altcoins are offering even deeper discounts.

You do not want to be caught bearish or sidelined going into this stretch. Time and time again, investors who wait end up buying higher or missing the move altogether. The setup is clear, and the playbook has not changed.

And we have not even talked about November yet. With an average return of 40.5%, that discussion is for the next Rake Review

In the News:

In the News:

FTX Creditor Payouts Underway at Discounted Rates:

FTX has announced the third round of creditor repayments, with $1.6 billion set to be returned to users. These repayments are based on the 2022 valuations of the lost assets, not current market prices.

To illustrate:

- Bitcoin: $30,000 per BTC

- Solana: $30 per SOL

- Ethereum: $3,900 per ETH

This means anyone who lost 1 BTC will only receive $30,000, even though Bitcoin trades significantly higher today. For Bitcoin and Solana holders, the haircut is substantial. Ethereum holders are slightly better off, given ETH has largely moved sideways over the past few years.

What matters now is what recipients decide to do with the funds. Some may take the opportunity to re-enter the market, others may remain in cash. Either way, this fresh injection of liquidity has the potential to act as a tailwind for crypto. If even a portion of that capital flows back into Bitcoin or the broader market, it could help sustain the momentum heading into Q4.

Wall Street Embraces Tokenisation:

NASDAQ has announced that it has filed with the US SEC to allow tokenised trading of stocks and ETFs. This move has sparked a wave of optimism, providing confidence that traditional finance is beginning to incorporate Web3 elements into its offerings.

Tokenised equities would allow investors to purchase fractions of stocks, similar to how one can buy fractions of a Bitcoin. This is a key barrier being removed for smaller retail investors. If approved, this would further legitimise the crypto space and open the door for deeper institutional and traditional flows into digital asset ecosystems.

The pendulum has now swung the other way and there may be no turning back. If this gets the green light, expect a strong move in crypto markets as this narrative shift takes hold.

US Government Shutdown Imminent Amid Political Deadlock:

The month looks set to end with a US government shutdown, following stalled bipartisan negotiations over spending cuts, border security, and policy amendments. No continuing resolution has been passed, and prediction markets are now pricing in an 85% to 86% chance of a shutdown as lawmakers return to Capitol Hill amid heightened political tension.

A shutdown is a partial halt of non-essential federal operations, triggered when Congress fails to approve funding legislation. So what does this mean for markets?

Risk-on assets may face heightened volatility due to increased uncertainty, while risk-off assets such as gold are likely to benefit and rally. The real question is how Bitcoin reacts. Will it behave like a risk-on asset and see volatility, or will it begin to attract capital like a risk-off hedge and see an influx of liquidity as investors look to reduce exposure elsewhere?

Market Update:

Market Update:

Here is the fast five of what you need to know about the market in September 2025:

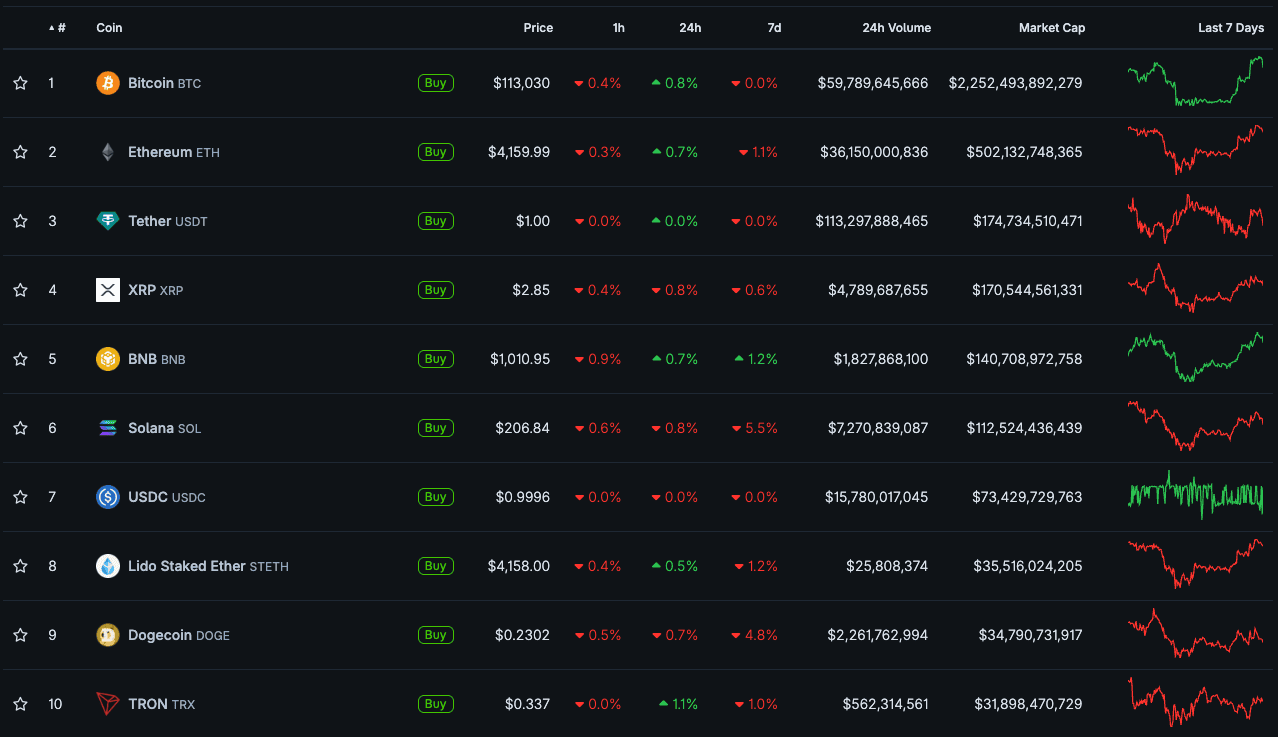

- Bitcoin increased by 5.21%

- Ethereum decreased by 4.43%

- The top 10 remained unchanged from last month

- BNB was the top performer in the top 10, climbing nearly 20%

- ASTER exploded onto the scene and quickly became a top 50 crypto project

Video of the month:

Michael Saylor on Bitcoin & Credit Markets: Bitcoin Treasuries Unconference Full Panel and Q&A

Education: Bitcoin’s Correlation: Gold, Equities, or Its Own Path?

There are several conflicting views when it comes to Bitcoin and what it actually tracks in the broader market. Some refer to it as ‘Digital Gold’, positioning it as an alternative safe haven asset, while critics label it the ‘Leveraged Nasdaq’ or treat it as just another tech stock.

So what does Bitcoin really behave like? Is it a risk-on or risk-off asset, or does it move entirely on its own terms? Let’s break it down.

Correlation in this context is measured as a 120-day rolling correlation. A value above 0 indicates a positive correlation, meaning both assets tend to move together. A value below 0 signals a negative correlation, where the assets move inversely.

Bitcoin and Gold

Let’s start with gold, given Bitcoin’s nickname.

Despite often being referred to as ‘Digital Gold’, the two assets have rarely moved in tandem over Bitcoin’s lifecycle. The highest recorded correlation between them came during the pandemic, where it peaked at 0.5. During that period, Bitcoin rallied 400% while gold climbed 67%, as investors fled to inflation-resistant assets.

Since then, however, the relationship has faded. Today, the correlation hovers between 0 and 0.1, and the long-term average since Bitcoin’s inception is close to 0. In short, the two assets rarely move together, despite the narrative.

The divergence has been especially clear in 2025. Gold is up nearly 50% year to date, solidifying its status as the world’s hedge asset. Bitcoin, meanwhile, has spent much of the year consolidating. The market still appears to classify Bitcoin as a growth asset, while gold remains the preferred hedge.

Bitcoin and the S&P 500

In Bitcoin’s earlier years, especially pre-pandemic, its correlation to the S&P 500 was minimal, and at times even negative. It moved largely on its own, often dictated by crypto-native catalysts such as the Mt Gox collapse, regulatory crackdowns from China, and market cycles driven by halving events and ICOs.

That changed during the pandemic. As central banks flooded the economy with stimulus, asset classes began to move together, and Bitcoin’s correlation with equities climbed. The peak came in May 2022 during a wave of rate hikes and geopolitical shocks, including the conflict in Eastern Europe, where both Bitcoin and the S&P 500 dropped sharply. At that point, correlation reached 0.68.

Unlike its relationship with gold, Bitcoin has maintained a moderately strong correlation with equities as it continues to mature. Institutional adoption has increased, and Bitcoin now reacts more consistently to traditional macro events. As of today, the correlation with the S&P 500 sits around 0.5.

Although the S&P 500 pushed to new all-time highs throughout September while Bitcoin moved sideways, the 120-day rolling correlation remains intact. If Bitcoin catches a bid in October, we could see that connection strengthen again.

Bitcoin Is Maturing, but Not a Hedge Yet

For most of its life, Bitcoin moved independently from both traditional equities and hard assets. But as the asset has matured, its relationship with equities, particularly the S&P 500, has become more apparent. Bitcoin now reacts more predictably to macro headlines like inflation, interest rate decisions, tariffs, and geopolitical conflicts.

That said, Bitcoin still has its own isolated catalysts — whether it is ancient wallets moving, major project failures, or sudden surges in institutional or government adoption. These are unique to the crypto space and can drive movement independently from traditional markets.

However, when it comes to broader market forces, Bitcoin currently behaves more like a risk-on asset. While the ‘Digital Gold’ narrative remains aspirational, and may eventually become reality, for now Bitcoin is more closely tied to equity market sentiment than it is to gold.

Written by Alexandar Artis

Start Your Brokerage Account

If you enjoyed this Rake Review, feel free to open an account and gain access to more proprietary research and work with your very own dedicated crypto broker.

No Advice Warning

The information in this newsletter is general only. It should not be taken as constituting professional advice from the author - Stormrake PTY LTD.

Stormrake is not a financial adviser and does not provide financial product advice. You should consider seeking independent legal, financial, taxation or other advice to check how the information relates to your unique circumstances. Stormrake is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by this newsletter.

Disclaimer

All statements made in this newsletter are made in good faith and we believe they are accurate and reliable. Stormrake does not give any warranty as to the accuracy, reliability or completeness of information that is contained here, except insofar as any liability under statute cannot be excluded. Stormrake, its directors, employees and their representatives do not accept any liability for any error or omission in this newsletter or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information provided in this newsletter is owned by Stormrake. You may not alter or modify this information in any way, including the removal of this copyright notice.Copyright © 2022 Stormrake Pty Ltd, All rights reserved